The continuation of the Red Sea diversions. elevated port congestion and a relatively low level of new ship deliveries in March continues to boost the containership charter market but has failed to revive the sagging freight market with the SCFI slipping by a further 2% last week to bring YTD losses to 48%. Carriers half-hearted bid to raise rates on 1 April is coming to a premature halt, with weak cargo demand keeping capacity utilization in check. Although the number blanked sailings on mainline routes increased in week 10, this was due more to port congestion related delays rather than pro-active capacity management by the carriers, with ample capacity returning to the market in the coming weeks. There remains no signs that carriers are willing to sacrifice market share to prevent further rate erosion, with EBIT margins still positive in the 1st quarter despite the recent rate declines.

Johnson Leung

Johnson Leung

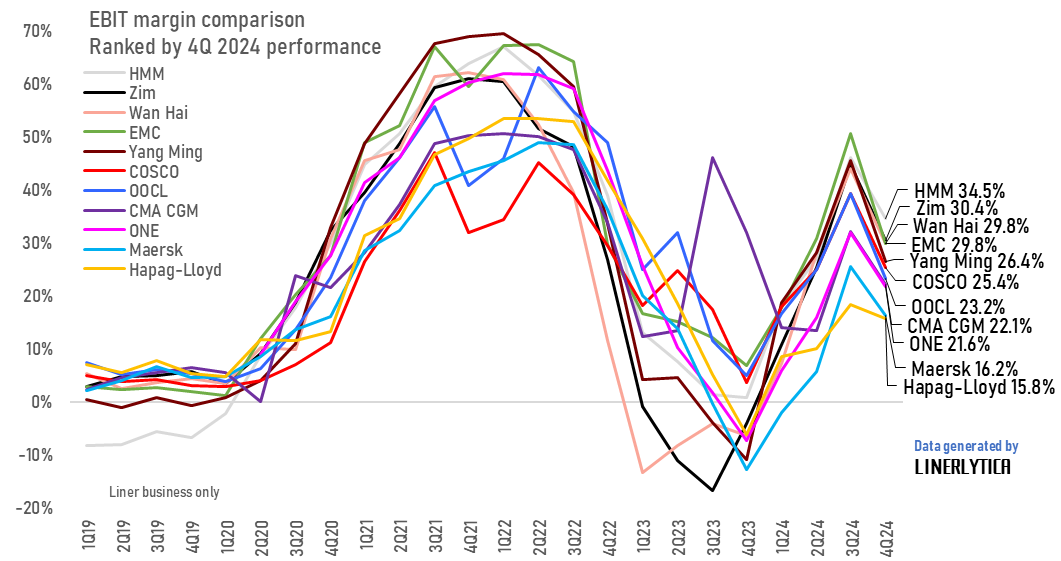

HMM & Zim top 4Q earnings margins while Hapag-Lloyd & Maersk stuck at the bottom

Carriers’ average EBIT margins remained healthy at 22% in the 4th quarter of 2024 despite dropping from the 3rd quarter average of 34%. Despite rapidly deteriorating spot freight rates, carriers will remain profitable in the 1st quarter of 2025, setting the stage for a fresh round of price competition in the remaining 3 quarters of the year. HMM and Zim topped the earnings league table with their higher East-West route exposure and spot business mix, while Hapag-Lloyd and Maersk continues to underperform due to their reliance on lower freight contract customers.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year