Carriers are finally taking action to curb capacity increases in their bid to reverse the recent freight rate slide, with MSC confirming the withdrawal of the transpacific Mustang service while also redeploying its largest 24,000 teu ships from the Asia-North Europe to the Med and West Africa routes. The OCEAN Alliance has also delayed plans to launch a new Asia-North Europe string in March, with Premier Alliance also expected to postpone the launch of 2 Transpacific strings scheduled to start in May.

These moves could trigger a correction in the containership charter market where rates have remained firm despite the recent sharp freight rate correction. Freight futures could also see a drop in the coming week as hopes of a rate rebound in March are dashed by carriers’ continued price slashing.

Johnson Leung

Johnson Leung

Containership charter market correction imminent

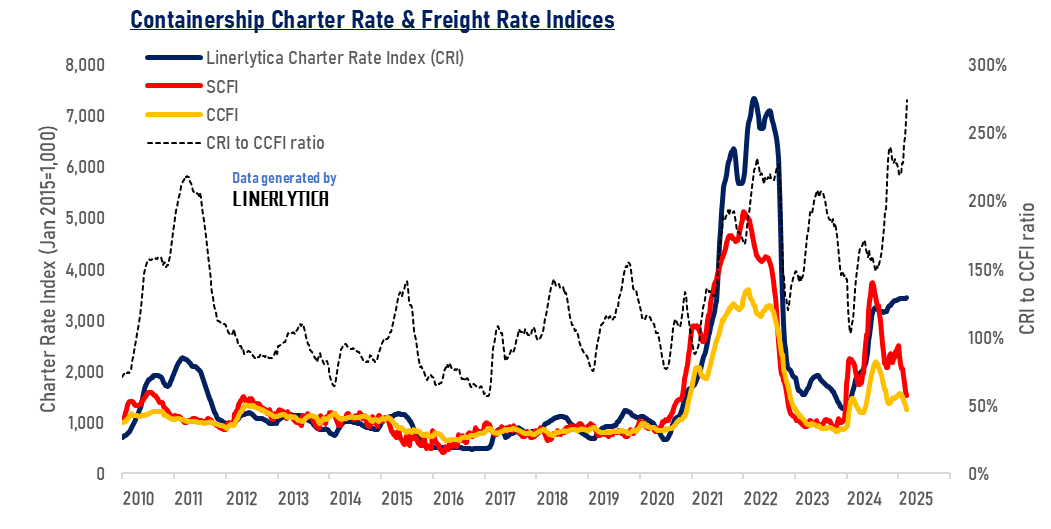

The widening disconnect between faltering container freight rates and the continued strengthening of containership charter rates is unsustainable, with the ratio of the charter rate index to the CCFI currently at a historic high.

Although charter rates and freight rates tend to move in tandem, there have been various periods in the past where they have diverged due to differences in demand and supply dynamics in the charter and freight markets. The Red Sea diversions have driven the widening divergence in the 2 indices since the beginning of 2024 but this could soon be reversed as carriers start to curb their appetite for additional ships amidst a weakening freight market.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year