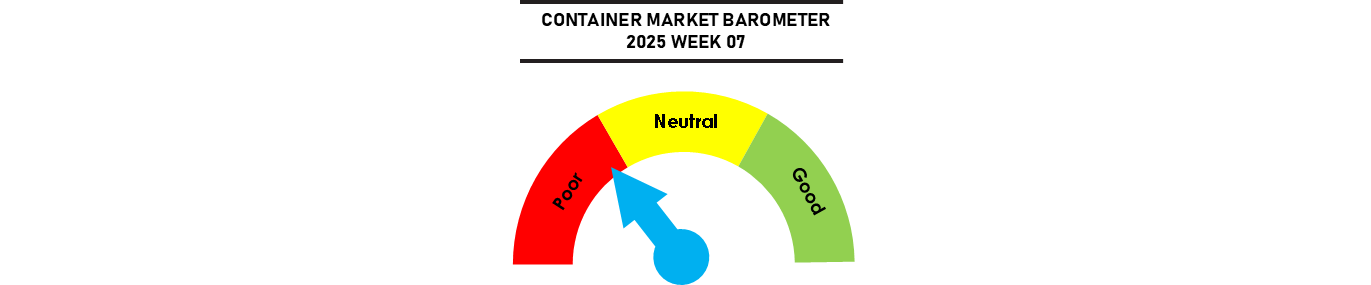

Despite the geopolitical headwinds and rapidly falling freight rates, the container markets is getting some relief from the continued vessel diversions from the Red Sea and worsening port congestion that continues to build up in Europe. The European routes are expected to see a rate rebound in March, with freight futures back in contango as forward rates in the next 6 months are expected to rise above their current levels.

But the momentum is weakening on the US routes as concerns mount over the impact of new tariffs that could see some of the initial Transpacific capacity deployment being rolled back. These challenges have not dampened MSC’s drive to grow as it continues to widen its lead over the rest of the market as it emerges stronger from the 2M breakup with a larger market presence as the gap between MSC and its nearest rival will soon breach 2m TEUs.

Johnson Leung

Johnson Leung

MSC emerges stronger after carrier alliance reshuffle

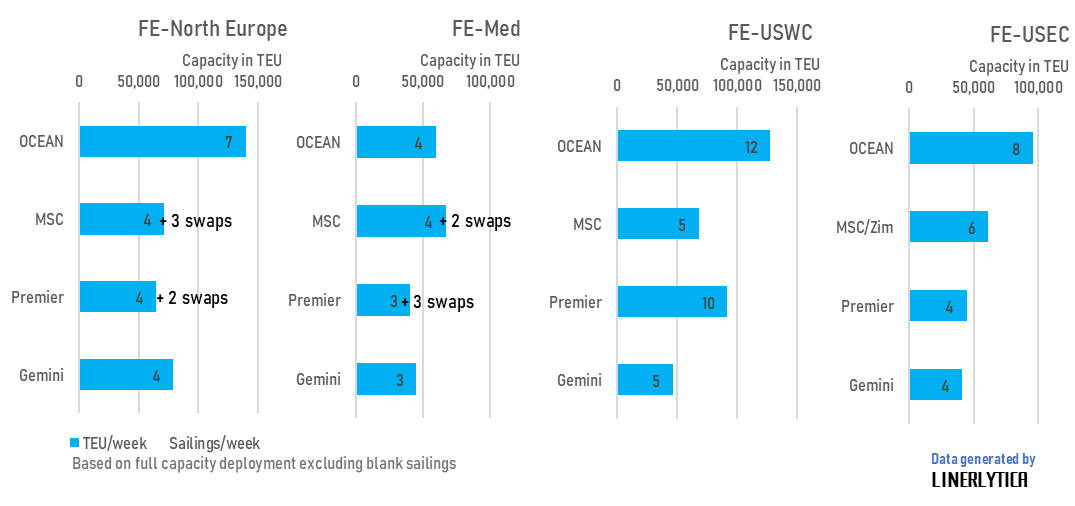

MSC will have better market coverage and a larger market share compared to the Gemini Cooperation despite operating as the sole independent carrier on the East-West trades following the alliance reshuffle in February 2025. MSC will be able to offer the same or a larger number of weekly sailings on all of the 4 main routes than Maersk and Hapag-Lloyd, using its self-operated services as well as selective partnerships with Premier Alliance on the North Europe and Med routes and with Zim on the US East Coast and PNW routes. MSC’s new East-West services’ deployment is fully filled with just one USWC Mustang service that remains without vessels named.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year