Container freight futures have rallied sharply, with December 2025 contracts surging by 53% over the past week as hopes for an early return of containerships to the Suez route fade. Since the 19 January ceasefire agreement in Gaza, there has been no ships diverted back to the Suez route with all main carriers retaining their Cape routing at least until March.

The potential return of the diverted Suez ships would release up to 7% of the global containership capacity with the resumption of slow steaming only able to absorb 1.5% of the surplus supply. With no signs of a swift return of the diverted ships, charter rates have resumed their tentative climb but freight rates remain under pressure with the SCFI shedding 7.3% while the CCFI fell by 6.0% compared to their pre-Chinese New Year levels. Carriers face an uphill battle to reverse the recent rate slide with cargo volumes still muted after the strong January cargo rush that had set new throughput records at key ports.

Johnson Leung

Johnson Leung

No early return to the Suez

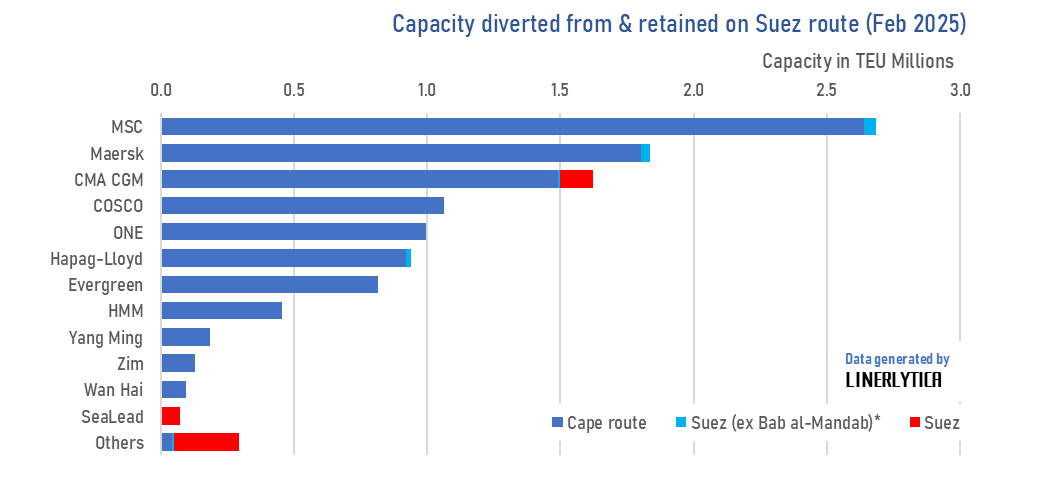

Containerships diverted from the Red Sea are not about to make an early return to the Suez, with all of the main carriers maintaining their Cape of Good Hope routing until March based on Linerlytica’s survey of all ships deployed on Suez-related routes. MSC, Maersk and Hapag-Lloyd are deploying a limited number of ships on Suez transits but these ships turn around at Jeddah and do not pass the Bab al-Mandab Strait. CMA CGM remains the only main carrier that is using the Suez/Bab al-Mandab route, although that is mainly limited to services serving Lebanon and only account for 8% of its total Suez-related capacity. Several smaller carriers including SeaLead, Safetrans, Messina, FESCO, M-Line, Akkon, OVP, Uniglobal and C-Star are using the Suez route primarily for the Black Sea, North Africa and Baltic Sea trades, but these niche operators account for less than 5% of the total capacity deployed.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year