The spectre of the Red Sea reopening following the ceasefire in Gaza weighs heavily on the containership sector, with up to 7% of the global fleet potentially coming back to market within the next 3 months. Freight rates have continued to tumble ahead of the Chinese New Year holidays with carriers still slashing rates while the SCFI recorded its first YoY drop last week, marking a tipping point for the market. EC freight futures continue to tumble with rates expected to drop by a further 55 to 65% over the next 12 months.

Although the containership charter market has held up until now, a reversal is looming with up to 2m TEU of vessel capacity expected to return to the market when the Red Sea diversions end. US sanctions against Chinese built ships and potential import tariff increases continue to cloud the outlook, with market sentiment turning more gloomy.

Johnson Leung

Johnson Leung

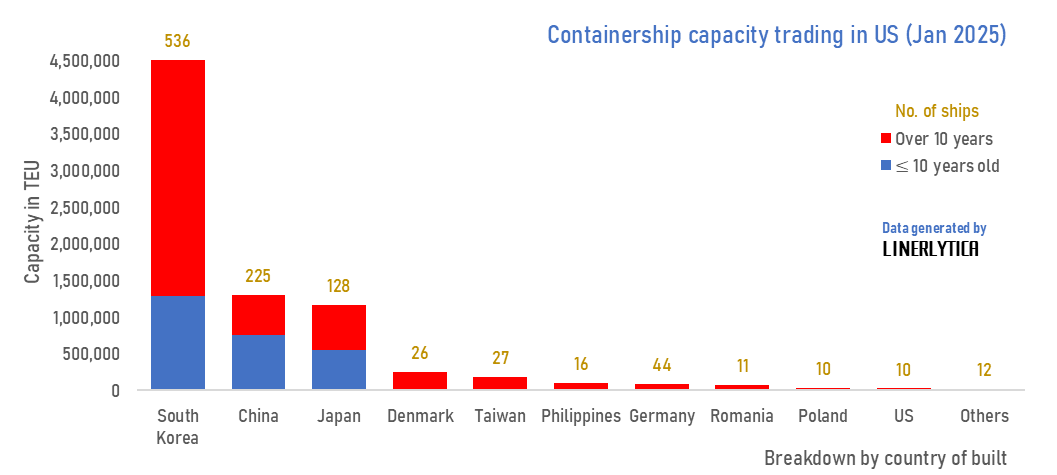

Potential US sanctions against China would hit 17% of US-bound ships

The US Trade Representative (USTR) concluded its investigation of China’s shipbuilding industry on 16 January 2025 and warned of further action to address what it deemed as unfair dominance of the sector. Based on Linerlytica’s analysis of all containerships currently trading in the US, Chinese built ships account for 225 units out of the 1,045 ships currently deployed in the US (excluding Jones Act trades) compared to just 10 ships that were built in the US. In TEU capacity terms, Chinese ships account for 1.29m TEU or 16.8% of the total capacity deployed, compared to just 23,200 teu (0.3%) that were built in the US. Ships built in South Korea remains as the largest source of ships trading in the US but South Korean shipyards have lost their leading market position to China which accounted for 66% of the total capacity of new containerships ordered since 2020.

(See page 2 for the fleet breakdown of carriers operating in the US - subscription only)

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year