As the market approaches the end of 2024 amidst increasing uncertainty given the prospect of another US East Coast port strike, looming US import tariff hikes and potential disruptions from the new alliance reshuffles, there are some positive developments for carriers who have managed to reverse the recent freight rate slide to keep 4Q rates above the 2Q levels. This will allow carriers to negotiate the new 2025 contract rates on a firmer footing despite the market uncertainties.

The positive momentum will continue into January with cargo demand expected to remain firm ahead of the Chinese New Year holidays and front loading before the inauguration of the new US President.

Full year fleet growth in 2024 will exceed 10% with 2.87m teu already delivered this year with just 2 more weeks to go before the year closes.

Johnson Leung

Johnson Leung

2024 ends on a positive note for carriers with freight rate rebound

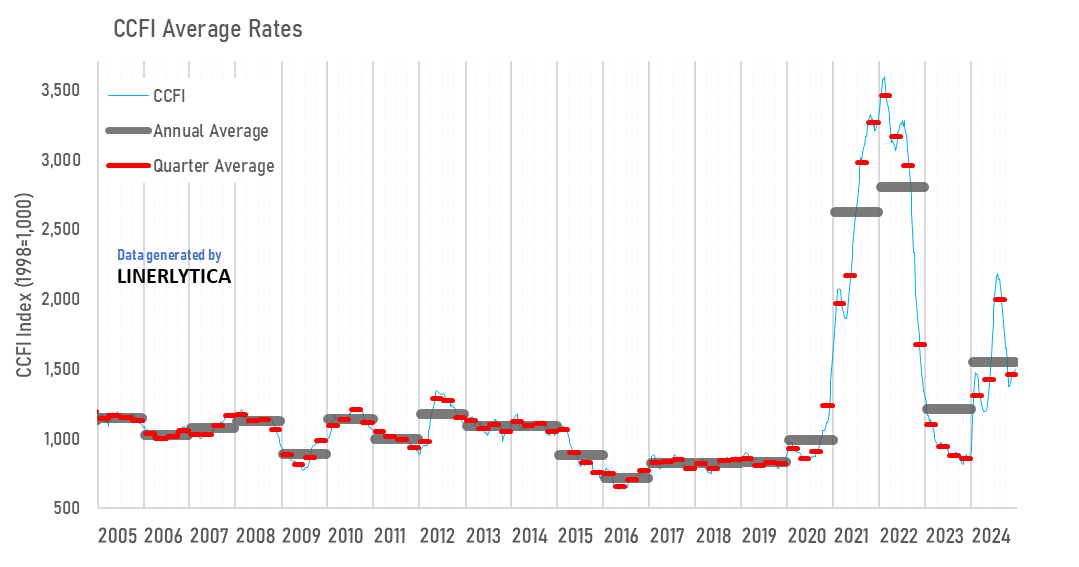

Both the CCFI and SCFI rebounded last week with carriers successfully reversing the recent slide in freight rates with Asia-Europe rates still holding on to most of their recent gains while Transpacific rates are staging a late rally amidst growing USEC port labor tensions and the threat of rising trade tariffs. Average CCFI rates in the 4th quarter is holding just above the 2nd quarter levels which will ensure that carriers’ earnings will remain healthy in the last quarter of 2024 with carriers’ average EBIT margins projected at 20%.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year