It was a mixed week for container freight rates with carriers able to hold on to their early December rate gains on the Asia-Europe, Middle East and Latin America routes but continued to lose ground on the Transpacific. Price competition on the transpacific route remains very keen with none of the main carriers willing to give up market share ahead of the alliance reshuffle in February even as newcomers such as Hede, SeaLead and TS Lines continue to pile into the market. Non-alliance carriers including Zim and Wan Hai have also increased their exposure on the route which remains lucrative despite the sharp rate correction that has erased 43% from the SCFIS USWC index in the past 4 weeks alone.

Transpacific rates are expected to strengthen in the coming weeks with the threat of another USEC port strike and front loading ahead of new US import tariffs could provide support for a fresh round of rate hikes. Charter market capacity remains very tight with several carriers still seeking tonnage ahead of the launch of the new alliance networks in February.

Johnson Leung

Johnson Leung

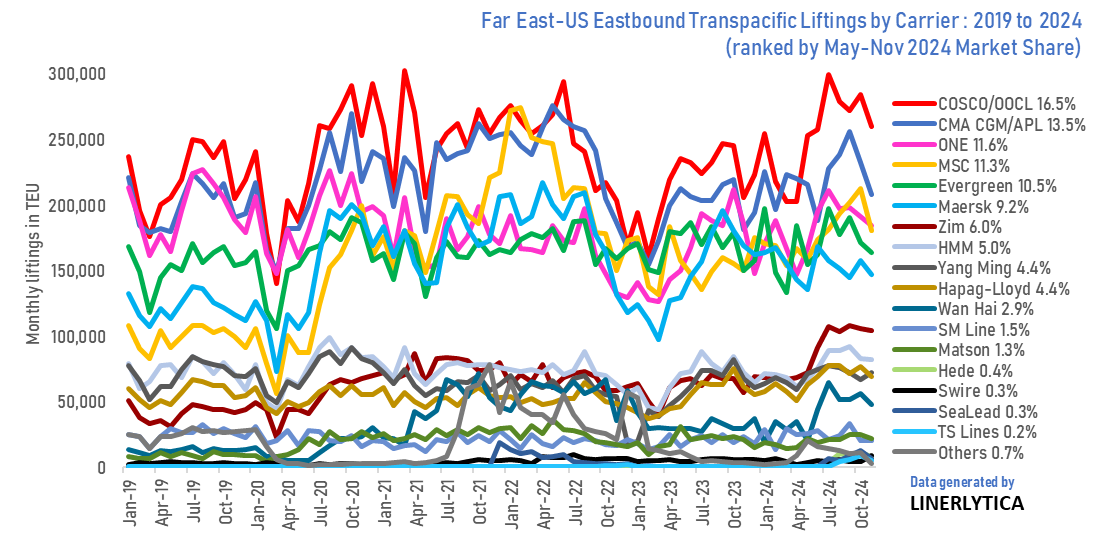

COSCO retains transpacific volume lead

COSCO remains the largest carrier on the Transpacific market, with a 16.5% share of total container volumes shipped on the Far East-US route for the 2024 contract season from May to November 2024. COSCO’s larger capacity share on the US West Coast allowed it to dominate the market compared to their European rivals (CMA CGM and Maersk) who deploys a larger proportion of their capacity on the US East Coast.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year