Container freight rates are still on track to stage a December rally, although initial gains on the Asia-Europe, Middle East and Intra-Asia routes have been tempered by continued weakness on the Transpacific and Oceania routes. Carriers’ efforts to push ahead with various rate hikes in November and December have stemmed the rate reductions of the previous 3 months, giving the carriers an improved bargaining position ahead of the new contract negotiations for 2025.

Carriers appetite for new tonnage continues to push charter rates higher. Apart from raiding the depleted charter market for additional tonnage, carriers have returned to the newbuilding market in droves with Maersk confirming a 20 ship order on top of additional charter deals as it tries to narrow the self-created gap with MSC. The orderbook ratio has rebounded to 27% from 20% in June on the back of more than 3.8m teu of new capacity that has been ordered in the last 6 months alone.

Johnson Leung

Johnson Leung

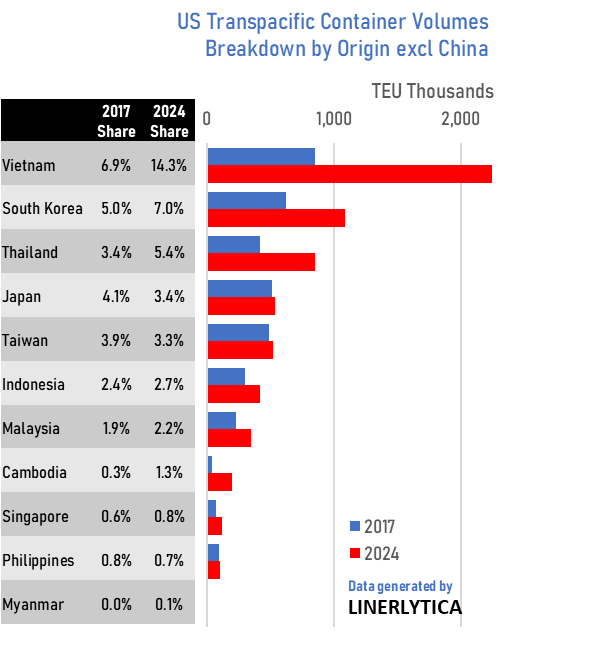

Vietnam, South Korea and Thailand set to profit from new Trump tariffs

Containerised cargo imports into the US from Asia have continued to grow over the last 7 years despite the introduction of US import tariffs since 2018.

Overall cargo growth grew by 3.5% on a compounded basis between 2017 and 2024 with all Asian origins recording positive cargo growth, including China that posted growth of 0.8% during the period.

Although China’s share of total US imports from Asia decreased from 70.4% in 2017 to 58.9% in 2024, it remains the largest origin country of container cargo to the US. Other Far East Asia origins recorded mixed performances with Vietnam, South Korea, Thailand and Cambodia generating the largest growth in volumes and market share gains.

Japan, Taiwan and Philippines saw their market share shrink, while Indonesia, Malaysia and Myanmar only recorded marginal gains as they failed to capitalize on China’s losses during the last 7 years.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year