The ILA dockworkers’ strike will be pivotal for the container markets in the coming weeks, as it will determine the direction that freight rates will take in October. The SCFI has dropped by 33% since its last peak on 5 July and remain under pressure after 2 consecutive 8% WoW declines. Cargo volumes have weakened ahead of the Golden Week holidays, with no signs of a pre-holiday surge. Capacity utilisation levels have slipped but carriers are more interested in expanding their roll pools ahead the Chinese holidays which would only prolong the spot rate free fall. This will be exacerbated by the carriers’ unwillingness to cut capacity ahead of the new alliance reshuffle in February 2025, with Maersk in particular still securing charter tonnage in order to meet their vessel shortfalls.

Only an extended strike on the US East Coast can lift the flagging freight market, with up to 15% of global capacity potentially affected if the strike lasts for an extended period.

Johnson Leung

Johnson Leung

Brace for USEC port strike

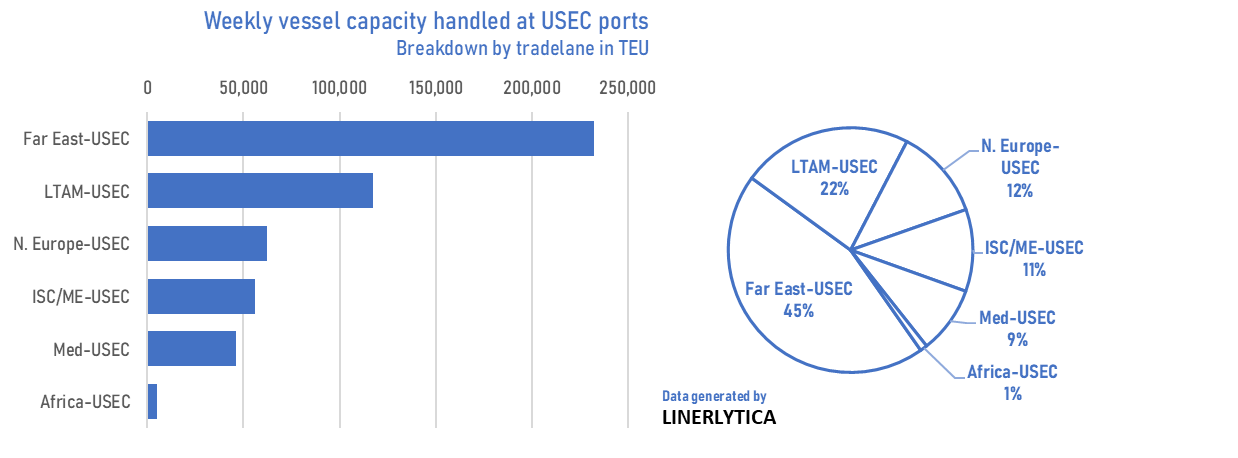

A coastwise strike at US East and Gulf Coast ports now looks certain to start on 1 October 2024. The 14 ports controlled by the ILA handled 28.4m teu of containerised cargo in 2023 or almost 550,000 teu each week. For each week that the strike continues, it would hold up 1.7% of the global containership fleet, with an indefinite strike expected to affect over 4.5m teu of the fleet, accounting for 15% of the total containership capacity.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year