Carriers are pushing for a mid-August rate hike to the US West Coast in an attempt to reverse the recent rate slide on that route. The carriers’ resolve will be keenly tested as recent capacity additions on the Asia to US West Coast and Mexico routes have tilted the supply-demand balance on the previously tight market with capacity utilisation falling despite strong peak season cargo demand. The carriers’ ability to hold Asia-Europe rates last week gave the freight futures market a much needed boost as forward rates for 2025 traded sharply higher at the start of this week after their recent 3 week correction.

Global capacity utilisation continues to trend 2% higher than 2023 despite the 10.4% growth in global containership supply in the last 12 months. Container cargo volumes grew by 7.4% at the 10 largest container ports in the 1st half of 2024, with the carriers’ ability to keep the freight rate momentum up largely dependent on a continuation of the positive cargo trend in the 2nd half of the year.

Johnson Leung

Johnson Leung

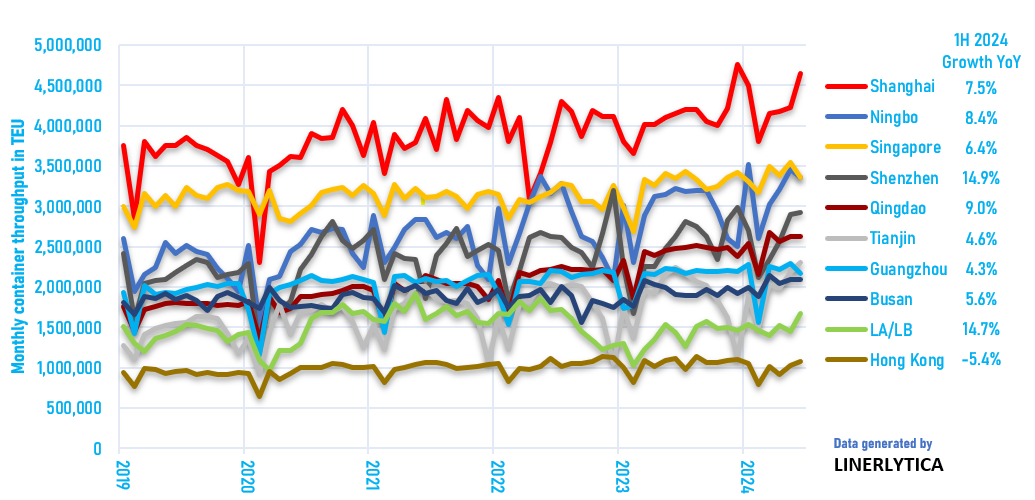

Container ports record strong volume gains in 1H 2024

Rising geopolitical tensions have not dampened container trade growth in 2024, with 10 of the world’s largest ports reporting combined gains of 7.4% in the first 6 months of the year. Chinese ports recorded particularly strong gains, led by Shanghai (up 7.5%), Ningbo (up 8.4%), Shenzhen (up 14.9%) and Qingdao (9.0%) with Hong Kong the only main port to record negative figures during the first half. Los Angeles/Long Beach rebounded with a 14.7% gain with June notably up by 16.8%. Singapore also recorded a gain of 6.4% bu slipped to 3rd position in June due to omissions by carriers to avoid port congestion. The strong performance is expected to persist through the 2nd half of 2024, with full year global container volume growth estimates revised upwards to 5.4%.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year