Rising port congestion has added further to the woes of the over-stretched container market that is already reeling from a shortage of container equipment and vessel space. The global port congestion indicator hit the 2m teu mark, accounting for 6.8% of the global fleet with Singapore becoming the new congestion hotspot. The SCFI has jumped by 42% in the past month, with further gains to follow in June as carriers are adding new surcharges and rate hikes.

Carriers have been forced to secure new boxes and vessel charters beyond September after their initial hesitation to commit too far ahead in the event that demand would falter after the summer peak season. Carriers have retained their cautious full year outlook with Zim the last of the main carriers to release 1Q results last week but market signals are extremely bullish at the moment mirroring the phenomenal rate increases that started in 2021 and continued until the end of 2022.

Johnson Leung

Johnson Leung

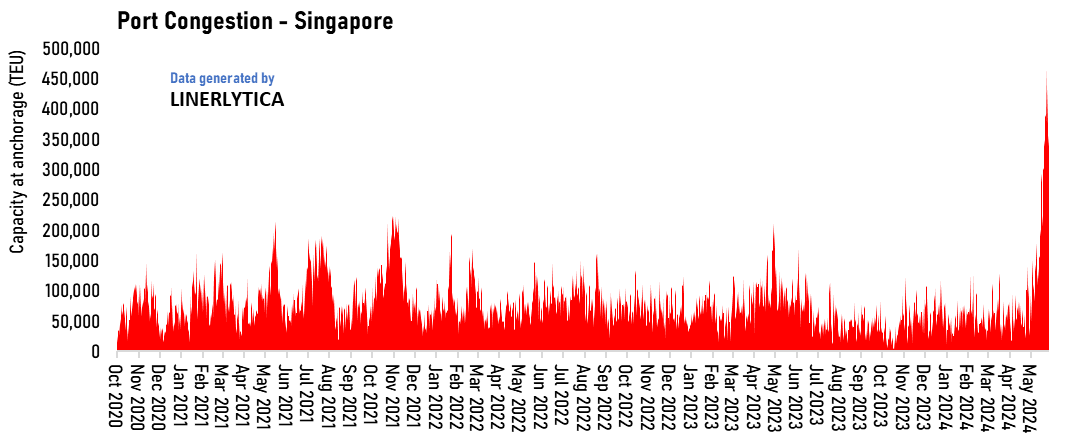

Singapore port congestion reach critical levels

Port congestion has returned to haunt the container markets, with Singapore becoming the latest chokepoint. Berthing delays at the world’s second largest container port of up to 7 days with the total capacity waiting to berth rising to 450,000 teu in recent days. The severe congestion has forced some carriers to omit their planned Singapore port calls, which will exacerbate the problem at downstream ports that will have to handle additional volumes. The delays have also resulted in vessel bunching which are causing spillover congestion and schedule disruptions at downstream ports. The rise in port congestion has taken more than 400,000 teu of vessel capacity out of circulation in the last week alone with a further escalation in the situation expected in the coming month.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year