Market panic over tightening vessel space availability has sent the SCFI to its highest level since September 2022, rising by 18.8% after last week’s holiday break to hit a 20-month high. Unlike the surge in January this year when the rate hikes were largely limited to the Red Sea affected routes, the gains are more broad-based this time with sharp rate hikes on all long-haul routes on the back of a strong rebound in demand ahead of the summer peak season.

Carriers are fanning the panic with Maersk claiming that capacity loss on the Asia-Europe and Med routes has reached 15-20%. Although the effective capacity situation is not as dire as the carrier suggests, the strong demand has taken the market by surprise with box equipment and vessels also in short supply. New dry box production surged to 520,000 teu in April alone, 3 times higher than the 2023 monthly average with new factory production fully booked until the end of July.

Johnson Leung

Johnson Leung

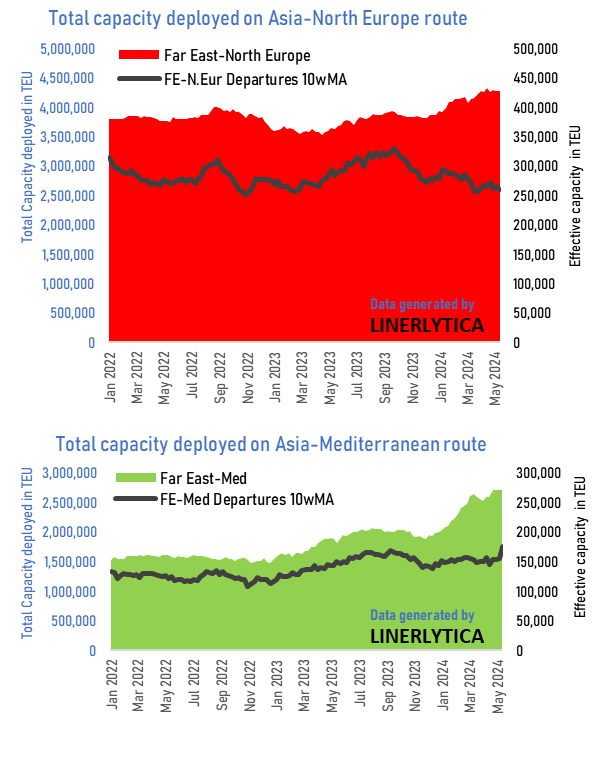

Asia-North Europe capacity loss offset by capacity increases to the Med

Effective capacity to North Europe based on actual vessel departures from Asia has decreased by 5.1% compared to a year ago due to the longer route taken by the majority of vessels via the Cape of Good Hope despite the deployment of 17.8% more vessel capacity on the Asia-North Europe route.

In contrast, effective capacity on the Asia-Med route is up 10.5% despite the Cape diversions as total capacity deployed on this route has jumped by 49.1% compared to a year ago.

Contrary to Maersk’s claims of an industry-wide 15% to 20% capacity loss on the Asia-Europe/Med routes, aggregate capacity is actually 0.3% higher in effective terms compared to a year ago as the total vessel capacity deployed on the 2 routes has increased by 28% from 5.45m teu to close to 7m teu currently.

1.2m teu in additional capacity have been added within the last 5 months alone due to the Cape diversions. The majority of the incremental capacity or 0.8m teu has gone to the Med as freight rates to the Med have enjoyed a 30-50% premium over North Europe, although the gap has narrowed recently.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year