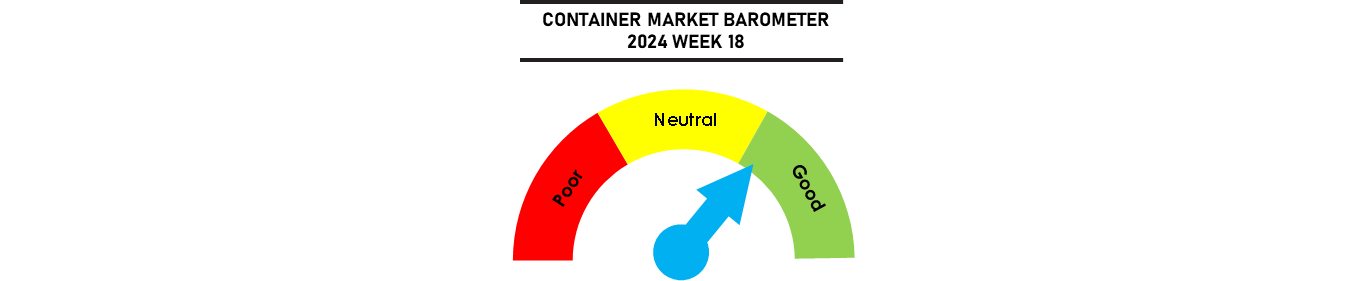

Freight rates are rising sharply across the board with the SCFI gaining 9.7% last week, erasing almost all of the spot rate declines since 1 March as carriers capitalised on the tightening capacity situation. Freight demand has risen ahead of the 1 May Labour Day holidays in China and increased number of blanked sailings next week with bookings also boosted by pre-GRI front loading before the higher rates take effect from 1 May.

Freight rates are expected to remain firm with another round of hikes planned in mid-May as container equipment and prompt vessels remain in short supply. New container boxes produced in China are fully booked until the end of June, while charter rates are rising sharply for ships above 1,700 teu. The vessel shortage has also forced COSCO to temporarily withdraw one of OCEAN Alliance’s Asia-North Europe strings, but freight futures retreated at the start of this week on potential Hamas-Israel ceasefire risks.

Johnson Leung

Johnson Leung

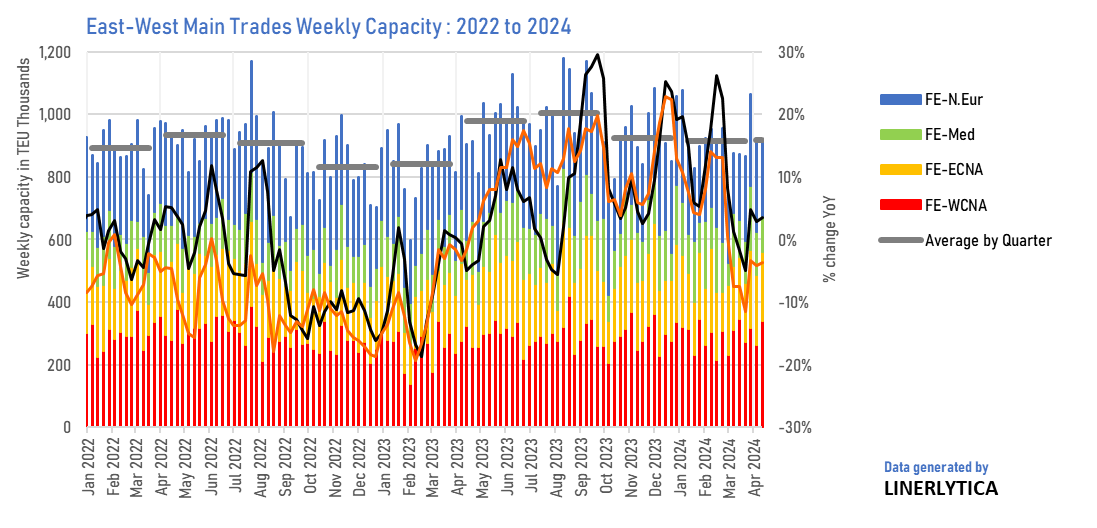

Effective capacity remains constrained despite record new ship deliveries

The containership fleet capacity currently stands at 29.37m TEU and will reach 30m TEU by the end of June this year. Although the nominal fleet growth has reached 10% YoY, effective capacity on the 4 main East-West trades has grown by only 3% this year as the vessel diversions to the Cape route due to the Red Sea crisis has absorbed most of the new capacity. At a global level, effective capacity on all 33 inter-regional linehaul routes tracked by Linerlytica has shrunk by -4% YoY, with reduced capacity deployed on the Red Sea/Middle East/Med routes dragging down the overall average despite the growth in the 4 main E-W trades.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year