The SCFI recorded its 3rd straight weekly gain last week and while the recent rate increases have been meagre, it will set the stage for a series of larger rate hikes in May that carriers have just announced. Capacity utilisation is tightening across all main trades on stronger market demand, which will aid carriers’ GRI efforts. Although new vessel deliveries continue at pace, the capacity shortage due to vessel diversions to the Cape of Good Hope as well as additional summer service deployments continue to soak up all available supply, with charter rates still rising for all vessel sizes apart from the smaller sectors below 1,200 teu.

Transpacific contract rates are settling 10-20% above last year’s levels, with the current spot rate levels pushing shippers to conclude negotiations at the higher rates. Asia-Europe freight futures also rallied last week with rising conviction that carriers will be able to hold the May rate hikes.

Johnson Leung

Johnson Leung

USTR actions against Chinese ships will do little to help US shipbuilders

The United States Trade Representative (USTR) initiated an investigation on China’s maritime, logistics, and shipbuilding sectors on 17 April 2024 based on the petition filed by 5 US labor unions that alleged unfair policies and practices to undermine fair competition and dominate the market. Amongst the proposed remedies to address China’s dominance is a fee on vessels built in China that dock at US ports.

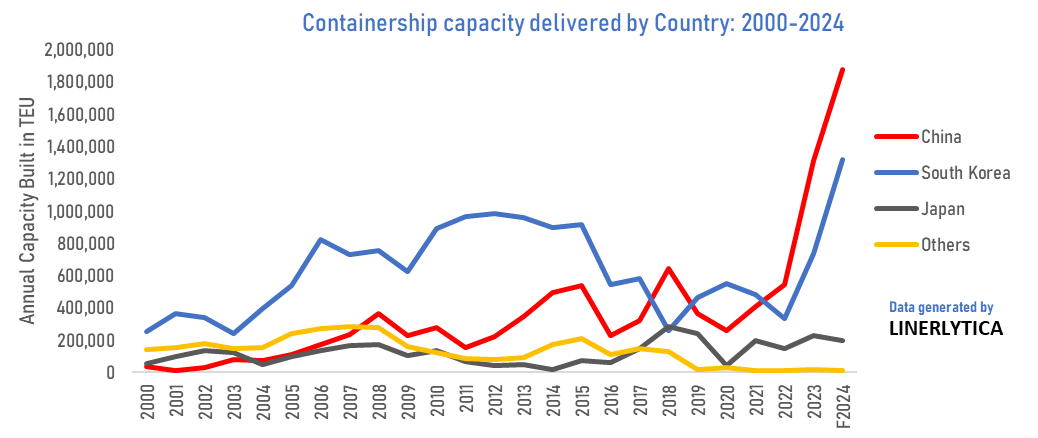

Although containerships built at Chinese shipyards account for only 27% of the current fleet capacity compared to 50% from South Korea and 10% from Japan, Chinese yards dominate the new vessel orderbook and account for 55% of current containership orders. In contrast, only 15 containerships have been built at US shipyards since 2000 and they cater solely to US domestic Jones Act carriers. Matson’s order for 3 units of 3,620 teu at Philly Shipyard for delivery in 2026-27 are the only ships currently on order at US yards. These ships were contracted in November 2022 at a total cost of US$1 Bn which is 5 times more than comparable ships built at Asian shipyards.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year