The Baltimore bridge incident failed to lift freight rates, with Transpacific rates still sliding after initial fears of disruptions to the US supply chains receded. The brief spike in both import and export spot rates from the US East Coast were quickly reversed as the Transpacific rate weakness pulled down the SCFI last week despite encouraging hikes on the Asia-Europe, Middle East and Latin America rates.

The Red Sea disruptions continue to drive a buoyant charter market where sentiment remains positive and demand still exceeding supply despite the large number of new ship deliveries with 12 ships delivered in the last week alone. Capacity across all routes are set to increase in April which will continue to put pressure on carriers’ recent rate gains and test their ability to hold rates ahead of the summer peak season.

Johnson Leung

Johnson Leung

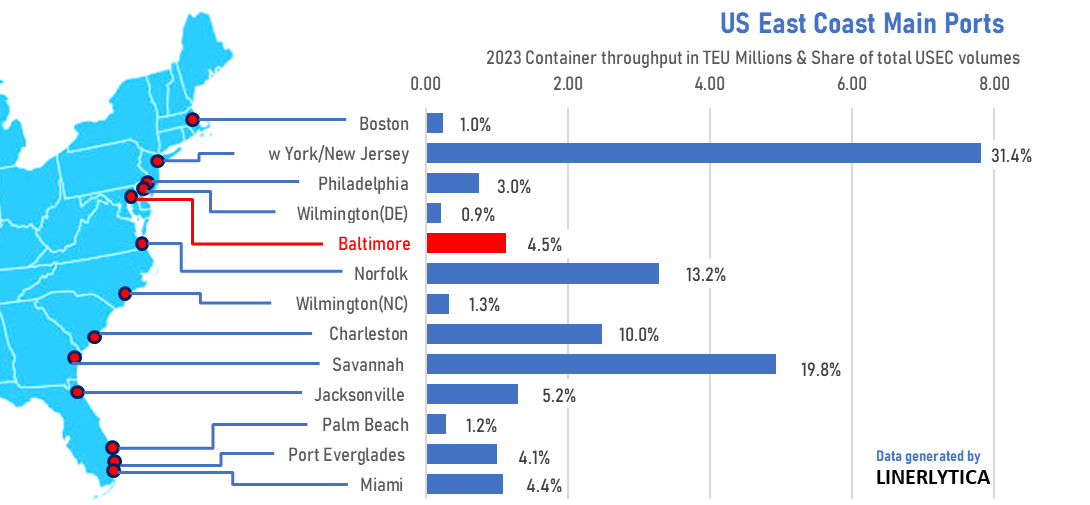

Baltimore port shutdown has limited impact on container volumes to US

The closure of the port of Baltimore after the 9,962 teu Maersk operated containership DALI struck the Francis Scott Key Bridge on 26 Match 2024 will not have a significant impact on container supply chain in the US. The port of Baltimore handled 1.12m teu of container cargo in 2023, accounting for only 4.5% of the total containers handled at the main ports at the US East Coast. There is sufficient container handling capacity at the neighbouring ports of Norfolk and New York where the cargo affected by the Baltimore port closure are currently being diverted.

Baltimore handles 11 regular services, with an average monthly handling volumes of 94,000 teu of which 50% are laden imports and 21% are laden exports with the remainder being empty containers, served mainly by the 4 largest carriers at the state of Maryland port - Maersk, MSC, Zim and Evergreen.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year