Conflicting signals abound in a market looking for fresh directions, with freight rates continuing to slide as the SCFI dropped by 4.7% last week bringing the cumulative decline to 15.8% since its January peak. However, charter rates continue to firm while second hand vessel prices are still rising as demand for tonnage remains high. The recent freight rate correction has not deterred new entrants, with another Chinese carrier set to launch a transpacific service in March.

The Red Sea diversions has already absorbed more than 1.26m teu of additional capacity, giving a boost to carriers’ earnings with the Red Sea dividend set to be reflected in the first quarter results. Taiwanese carriers have reported revenue gains of between 8% to 30% in the first 2 months of this year, in line with the SCFI and CCFI which are up 112% and 17% respectively YoY.

Johnson Leung

Johnson Leung

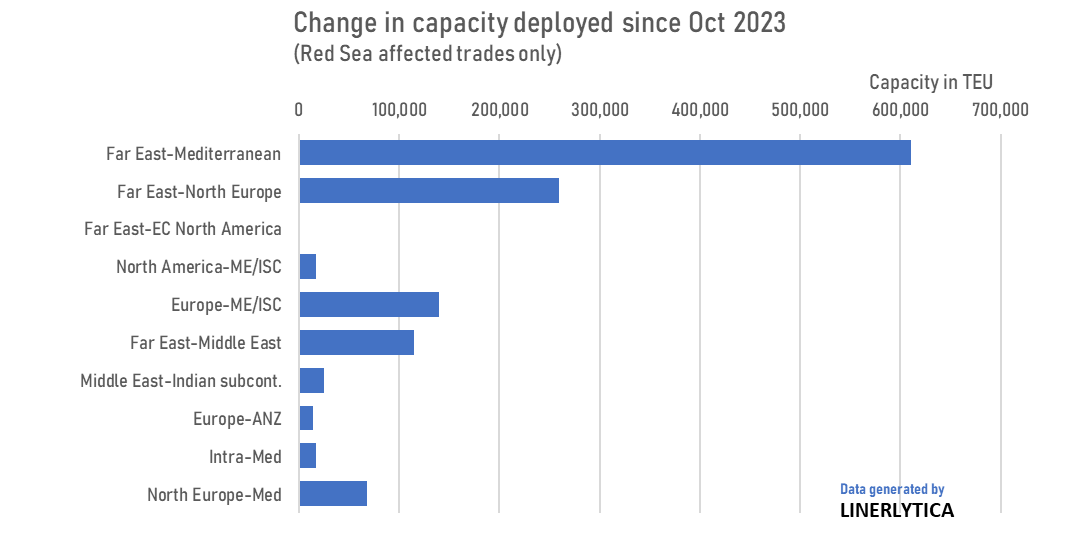

Red Sea crisis has absorbed over 1.2m of containership capacity

Total containership capacity deployed on trades affected by the Red Sea crisis has increased by 1.26m teu since October 2023, driven mainly by the vessel diversions to the Cape of Good Hope. The Far East-Mediterranean recorded the largest jump of 0.61m teu, accounting for half of the increased capacity over the period, followed by the Far East-North Europe route at 0.26m teu. The increased demand for tonnage has fully absorbed all of the new capacity delivered in the last 5 months, with additional requirements for another 400,000 teu of incremental capacity still to be fulfilled.

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year