The freight rate correction gathered pace after carriers failed to defend their pre-Chinese New Year gains with the SCFI shedding 6.2% last week. Although the Red Sea dividend remain in play with spot rates still 96% higher compared to December last year, cargo demand has not rebounded sufficiently after the Chinese New Year holidays to provide rate support with carriers unable to mount a serious 1 March GRI attempt on the transpacific route ahead of the crucial annual contract negotiations.

Charter rates are moving in the opposite direction, with the composite charter index rising by 5% last week reflecting the capacity shortage and positive sentiment amongst carriers still keen to secure additional tonnage even though some 300,000 teu is scheduled for delivery in March after new ship deliveries fell to just 194,000 teu in February due to the holidays in the Far East.

Johnson Leung

Johnson Leung

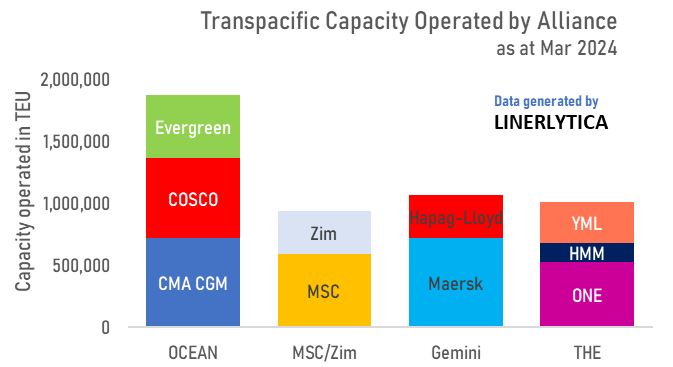

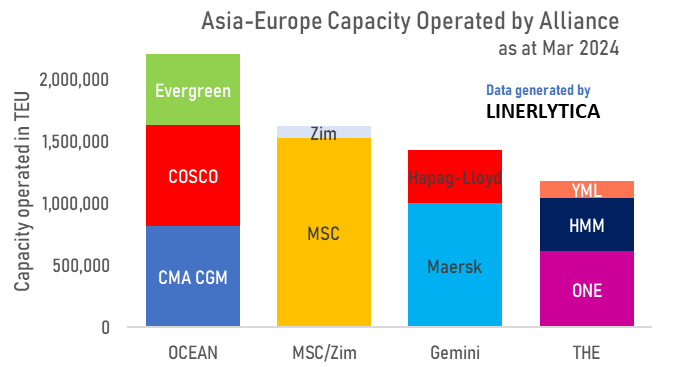

OCEAN Alliance extension leaves THE Alliance stranded

The OCEAN Alliance partners (CMA CGM, COSCO, OOCL and Evergreen) have extended their 10 year cooperation agreement that started in April 2017 for 5 more years until 31 March 2032. The move will cement the group’s dominant position as the largest global carrier alliance, with a significant lead over their rival alliances on both the Transpacific and Asia-Europe routes.

The move also leaves the remaining members of THE Alliance partners stranded as they will not be able to draw one of the OCEAN Alliance members to replace Hapag-Lloyd who will leave the alliance to join Maersk on the new Gemini Cooperation in 2025.

THE Alliance sans Hapag-Lloyd will be the smallest of the 4 global carrier alliances and will be particularly weak on the Asia-Europe and Transatlantic routes where they do not have sufficient capacity and market coverage to compete effectively with the rival alliances.

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year