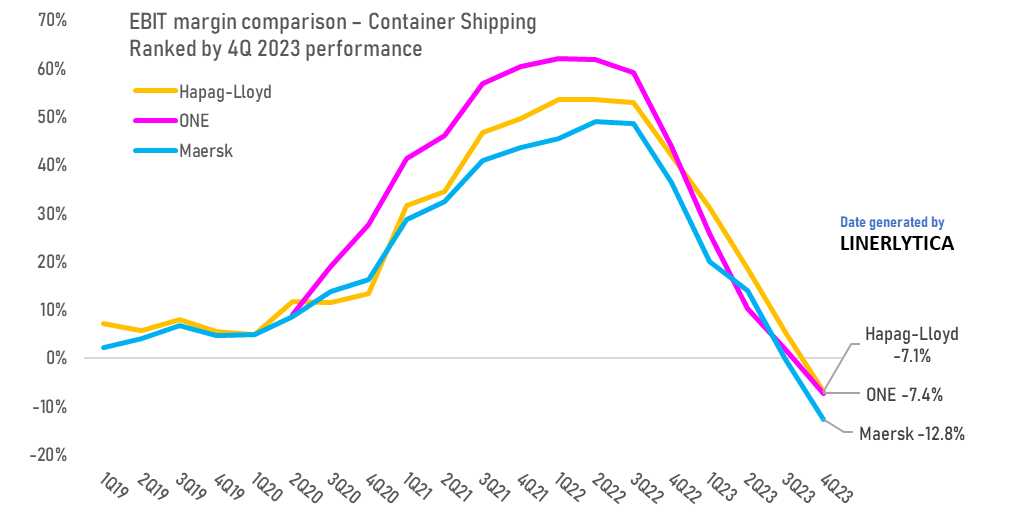

Despite Maersk’s best efforts at painting a pessimistic picture for the container shipping market, rates have retained most of their recent gains heading into the post Chinese New Year slack period. The SCFI and CCFI indices are 117% and 28% higher compared to the same period last year, which will help to reverse the carriers’ massive 4Q losses. Maersk’s underperformance compared to its liner peers has become more glaring, with its EBIT margins lagging by as much as 20% behind its closest rivals since 2020.

Charter rates have continued to firm, with Maersk ironically being the most active charterer accounting for almost one-third of recent market fixtures including forward fixtures for delivery into the 2nd quarter of 2024. Linerlytica’s charter rate index has risen by 27% since the Red Sea diversions started in mid-December and current rates are 65% higher than the 2019 average.

Johnson Leung

Johnson Leung

Maersk underwhelms with dismal 4Q earnings and 2024 guidance

Maersk blamed over-capacity for its record EBIT losses in 4Q but it failed to mask the fact that Maersk has continuously under-performed the market. Maersk reported EBIT losses of -$920m for its Ocean business with EBIT margins dropping to -12.8% in the 4th quarter of 2023, which is more than 5% lower than its liner peers that have announced their latest quarterly results.

It remains to be seen how long can Maersk investors tolerate the below-par performance which will continue in 2024 with Maersk expecting EBIT losses ballooning to -$5 Bn in the worst case scenari. Maersk continues to pursue logistics acquisitions and has confirmed a bid for Schenker despite its logistics services delivering EBIT margins of just 1.7% in the 4th quarter.

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year