Freight rates remain firm as the market entered the last week before the Lunar New Year holidays, led by transpacific rate hikes on 1 February that pushed rates to the US West Coast 267% higher than the same period last year. The Red Sea diversions have absorbed all of the excess capacity in the market, with the supply of vessel space and box equipment expected to remain tight in the next 2 months. Although the market will soften in the next 3 weeks with extended holidays in the main Far East origins, the Asia-Europe, Asia-US East Coast and Intra-Europe routes remain short of tonnage and charter rates have firmed as a result. Some carriers are willing to commit up to 6 months ahead of vessel delivery in a show of confidence that the current escalated market could last through most of this year. CMA CGM has started to reroute some of its Asia-Europe ships to the Cape after resisting the move for the last 2 months as tensions in the Red Sea continued to escalate.

Johnson Leung

Johnson Leung

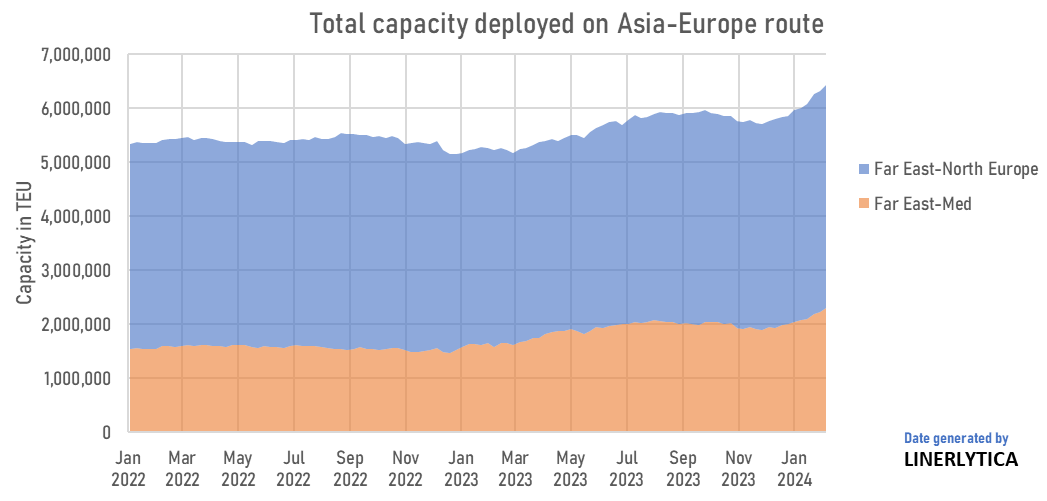

Capacity deployed on Asia-Europe routes at all-time high

Total containership capacity deployed on Asia to Europe routes have surged to a record high of 6.44m teu, up 23.3% compared to the same time last year. The surge is due entirely to diversion from the Suez to the Cape route since December 2023, with over 700,000 teu of additional capacity added to the trade in the last 2 months alone. 55% of the additional capacity has been absorbed in the FE-Med trades where transit times have increased by 10 days to the West Med and 18 days to the East Med while transit times to North Europe has increased by 7 days on average.

Apart from the direct impact on the Asia-Europe route, the Red Sea crisis has also created additional demand for Intra-Europe capacity which has increased by 24.8% year-on-year, with the largest increases seen on the intra-Med and North Europe-Med routes.

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year