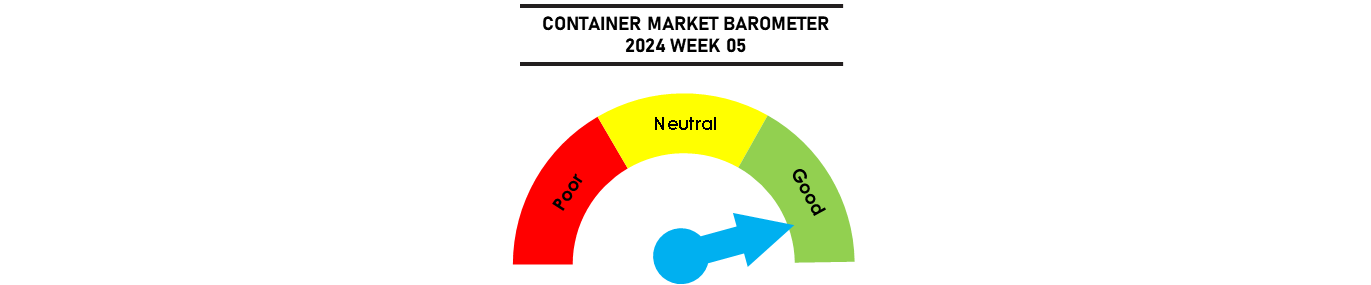

Spot freight rates have eased ahead of the Chinese New Year with the SCFI shedding 2.7% of its value last week, but average rates out of China are still rising as the CCFI rose by 8.9% with carriers able to consolidate their rate gains since the beginning of December. The composite CCFI has risen by 64% since over the last 8 weeks, guaranteeing bumper windfall gains for carriers in the 1st quarter of 2024 with carriers expected to retain most of their rate gains despite the post-Chinese New Year rate correction. Tight vessel supply amidst the rising demand has also lifted charter rates for containerships by some 15% since December, with the Red Sea diversions creating additional tonnage requirements across all sizes. Although new ship deliveries in January will exceed 300,000 teu with several ships still due to be delivered in the next few days, this has not been sufficient to cater for the increased demand with the current market barometer remaining very bullish.

Johnson Leung

Johnson Leung

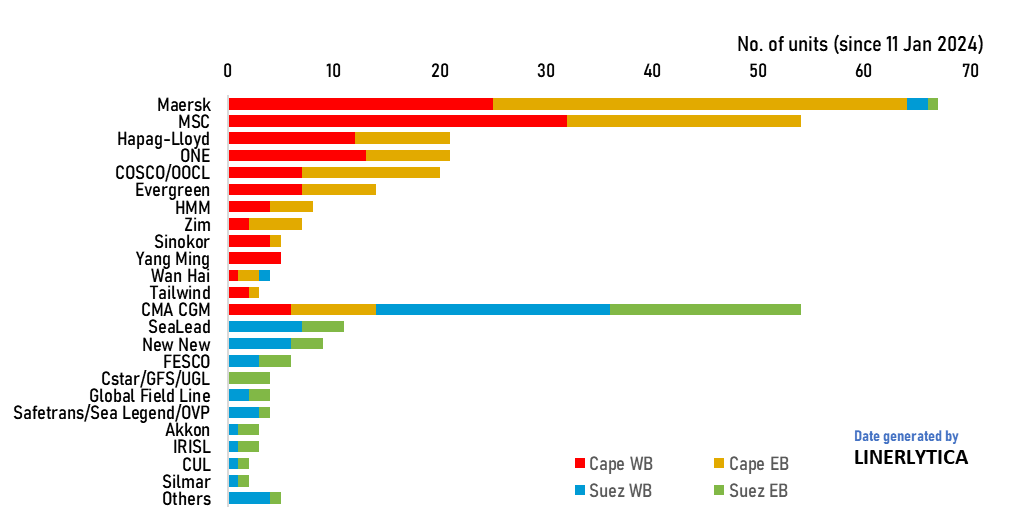

1 in 3 containerships remain on the Red Sea/Gulf of Aden route despite heightened risks

Maersk has withdrawn all of its ships on the Gulf of Aden including its US flagged ships on the MECL service connecting India/Middle East with the US East Coast following rocket attacks on 2 of its ships on 23 January. Despite the heightened security risks, CMA CGM has retained the Suez/Red Sea routing for its ships on the Asia-Europe/Med route, with only its USEC-Asia and Oceania services currently re-routed to the Cape route.

At least 19 other carriers serving the Asia to Med and Baltic trades are maintaining their Suez routing even after US and UK forces launched attacks on Houthi bases on 11 January, accounting for some 30% of all containerships that previously used that route. CMA CGM ships has received French naval escorts, while one Chinese carrier has cited Chinese naval escorts even though the main Chinese carrier COSCO has not sent a single ship on the Red Sea route since December.

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year