The 2M breakup will trigger another round of market instability as Maersk and MSC jostle for pole position on the East-West routes where they currently cooperate. While MSC will have sufficient new ship capacity by 2025 to fully replace Maersk’s current vessel contribution to the 2M network, an independent Maersk network will fall behind MSC, OCEAN Alliance and THE Alliance offerings.

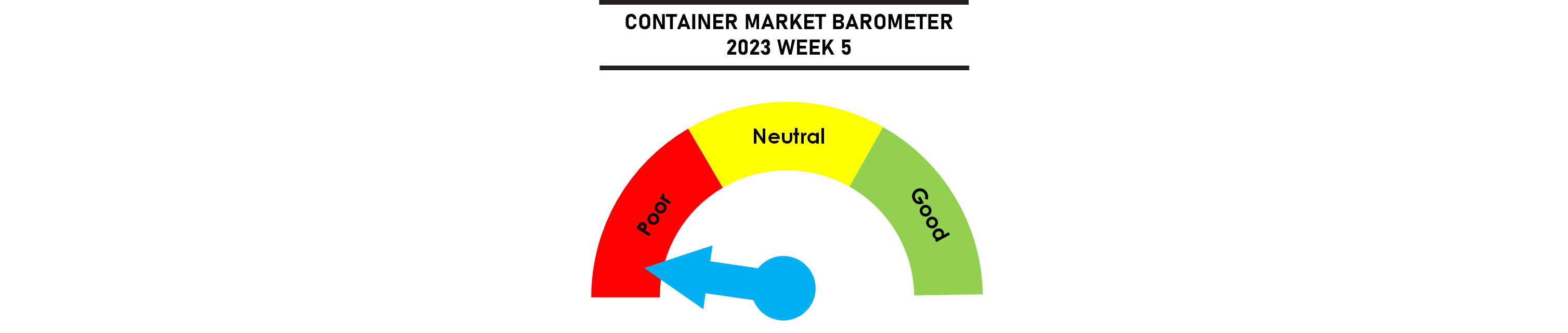

Freight rates are still dropping despite limited market activity in the Far East due to lunar new year festivities. More clarity is emerging on the deferred 2023 contracts on the Asia-Europe routes, with $1,500/feu the new market benchmark compared to contracts concluded earlier at above $2,000/feu as carriers come to terms with the new market reality.

Jonathan Lee

Jonathan Lee

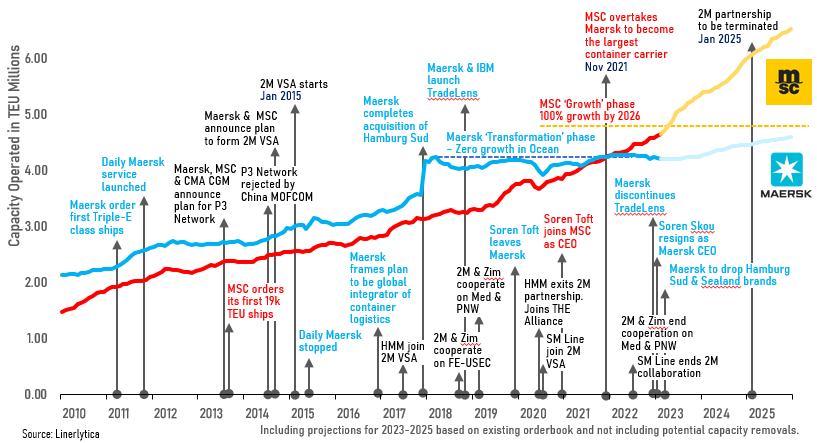

The timeline of how Maersk was outmaneuvered by MSC culminating in the announcement on 25 January 2023 that the 2 carriers will terminate their 2M partnership in January 2025. While Maersk dithered through strategic mis-steps including high profile flops such as Daily Maersk and TradeLens, MSC was resolute in building scale in its shipping business. Maersk had triggered the capacity race in 2011 when it ordered the first Triple-E ships but has been beaten at its own game by MSC who are set to be over 40% larger than Maersk by the end of 2025 based on their current orderbook. Maersk chose to build on its new strategy as a global integrator of container logistics and have spent over $5bn on a string of logistics acquisitions since 2018, but it allowed the big prize of Bollore Africa Logistics to slip into MSC’s hands.

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year