The SCFI surged by 14.8% on the back of the Red Sea turmoil to hit a 13 month high, with a looming capacity crisis set to erupt over the coming weeks as ships that were supposed to return to Asia from Europe and the US East Coast via the Suez are delayed by 2 to 3 weeks. This will coincide with the high cargo demand expected in the run up to Chinese New Year, with freight rates expected to remain elevated through mid-February backed by the tight space situation.

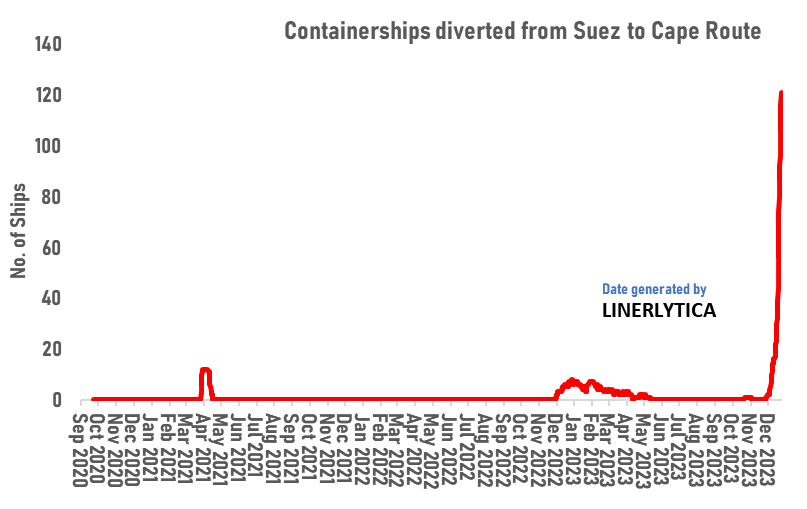

The number of containerships diverted from the Suez to the Cape Route has reached 125 units as at 24 December with a total capacity of 1.77m teu. Although Maersk said that it was preparing to resume Red Sea transits with the Operation Prosperity Guardian (OPG) in place, the majority of the affected ships are still proceeding on the Cape route.

Johnson Leung

Johnson Leung

Capacity crunch looms as diversions from the Red Sea hit record high

The number of containerships diverted from the Suez to the Cape Route has surged to 125 units compared to 44 a week ago, including 16 ships that turned back in the Red Sea to the Med after making their southbound Suez passage. The record number of diversions far exceeds the number of ships that were diverted during the EVER GIVEN incident on the Suez Canal in March 2021 when less than 20 ships were diverted. While the previous Suez blockage in 2021 lasted barely 7 days, the impact of the current diversions will take a longer time to unravel.

The majority of ships on the Asia-Europe and USEC via Suez routes are retaining their revised Cape routing as at 25 December 2023 with carriers still assessing the safety risks of returning to the Red Sea route.

Suez traffic has not stopped completely, with a limited number of containerships still making the passage over the past week including a small number of ships from Maersk, MSC, CMA CGM and Hapag-Lloyd under escort. Notably, several Asia-Europe micro-carriers serving Russian Baltic, Med and Black Sea ports including Akkon, CStar Line, E-Line, New New Shipping, OVP, Safetrans, SeaLead and Sinokor have continued to take the Suez/Red Sea route.

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year