The SCFI slipped to its lowest levels since May 2020, with further falls expected in the coming weeks as volumes remain lacklustre. Carriers are still unwilling to make decisive capacity cuts despite the rate slump and absence of cargo roll pools before the start of the Chinese Golden Week holidays on 1 October.

Maersk in particular have been singled out for giving heavy discounts on its spot pricing even as it continues to lose ground against its closest rivals with the gap to market leader MSC widening to over 1.2m teu while CMA CGM will snatch its no. 2 spot by 2026. The market impasse will last through the end of the year, with capacity across all main trades still rising even as global demand remains flat. The idle fleet remains immaterial at just 0.6% of the total fleet and while this will rise over the coming weeks due to blank sailing programs in October, it remains too low to turn the market around.

Johnson Leung

Johnson Leung

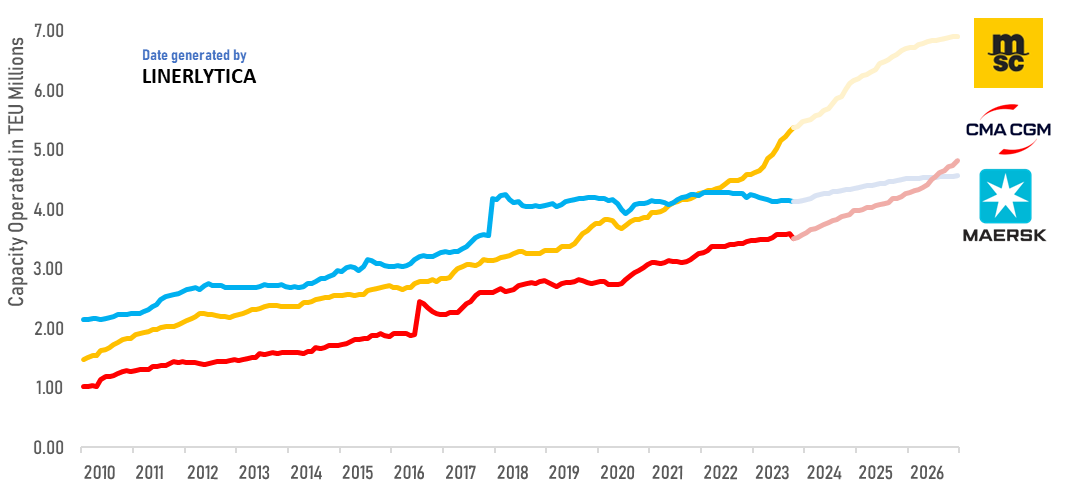

Gap between Top 3 carriers widen

MSC has extended its lead at the top of the carrier rankings, with its current fleet reaching 5.36m teu, up from 4.61m teu at the beginning of January. Newbuilding deliveries contributed 557,000 teu to the increase, with the rest coming from second hand vessel acquisitions and new charters. MSC has grown at an average rate of 83,000 teu a month, with its lead over 2nd place Maersk rising to 1.24m teu.

Maersk has seen its operated fleet shrink from 4.21m teu at the beginning of the year to 4.12m teu as it continues to downsize and will relinquish its no. 2 position by 2026 as CMA CGM tries to keep pace with MSC’s growth. CMA CGM has added to its newbuilding tally, with a fresh order made last week for eight methanol fuel units of 9,200 teu at Shanghai Waigaoqiao.

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year