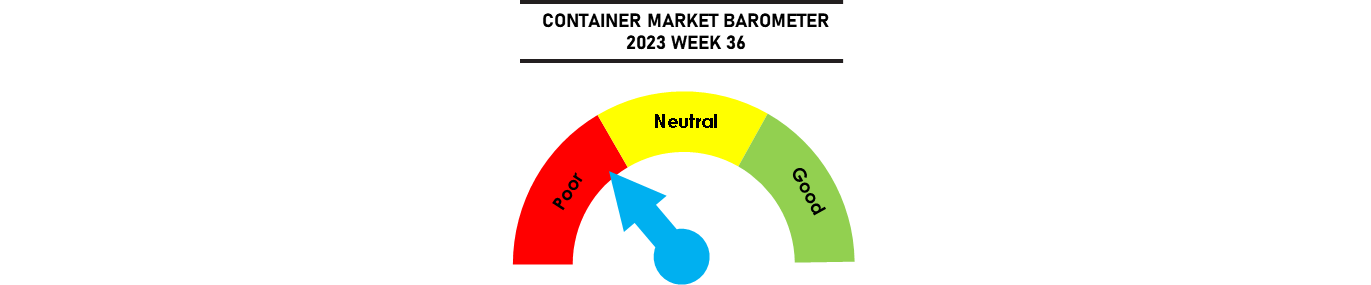

Freight rates have rebounded slightly following the 1 September rate increase that were applied on trades out of Asia to the US, Australia and India/Middle East but the gains are reversing as quickly as they are applied with carriers offering rate discounts. Asia Europe rates were severely battered due to continued capacity pressure with 3 ULCS units delivered over the past week alone as the pace of newbuilding deliveries is maintained at just below the 200,000 teu level in August with few signs of capacity discipline as scrapping activity remains muted while the idle fleet remains stubbornly low at just 0.5% of the fleet.

Rates will come under increasing pressure through September, with transpacific carriers already withdrawing peak season surcharges even before the Golden Week holidays in October. Belated attempts to blanks sailings from the end of September will do little to address the imbalance in the absence of concrete service withdrawals.

Johnson Leung

Johnson Leung

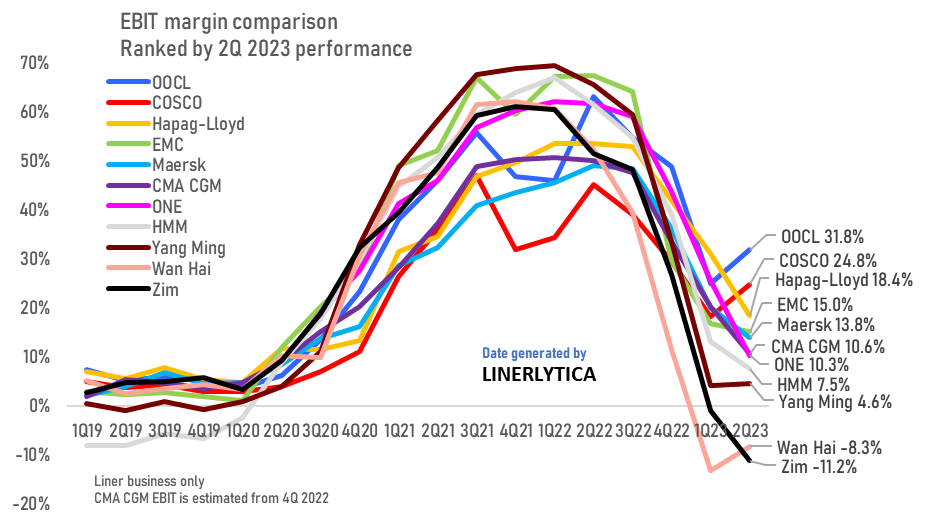

COSCO, OOCL and Wan Hai reverse earnings decline

Carriers reported a mixed 2nd quarter 2023 performance, with 3 carriers able to reverse their earnings decline despite the weak market conditions. OOCL and COSCO jumped to the top of the carriers earnings table with their outsized 2Q earnings despite weaker revenue and freight rates. OOCL and COSCO’s EBIT margins at 31.8% and 24.8% are more than 3 times higher than the average of the next 8 carriers which stands at just 6.7%. COSCO reported at the group level a $5.7 Bn improvement in its equipment and cargo transportations costs over the first 6 months of this year, which would have contained writebacks of provisions that the group had taken in 4Q2021 and 1Q2022 when both COSCO and OOCL recorded earnings dips.

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year