Market sentiment has turned negative again, with carriers unable to retain the recent rate increases as the SCFI slipped by 1.2% last week. The setback will make it harder for carriers to push for the next round of rate hikes in September, with no signs of capacity management in place.

The idle fleet remains low even as new ship deliveries continues apace. The mounting losses at Zim has forced it to rationalise capacity but its larger rivals are not following suit. Having pulled out its ships from the WCNA in June, Zim will also withdraw its ships from the Asia-Oceania routes from October. Zim has opted to take slots from MSC on both trades, allowing MSC to optimise its fleet even as it continues to pull ahead of their competitors. MSC’s lead over Maersk has widened further to 1.09m teu.

Johnson Leung

Johnson Leung

Zim pays price for market expansion gone awry

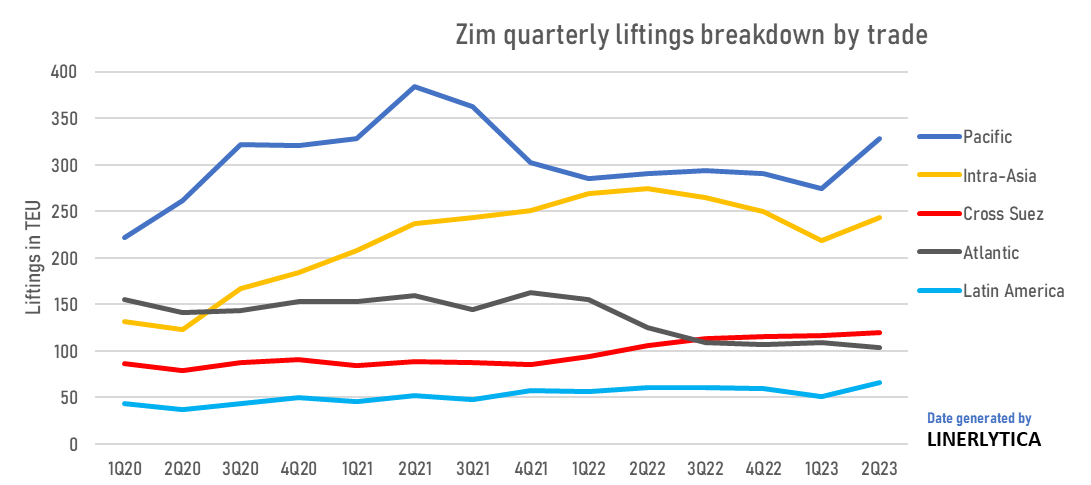

Zim recorded its worst quarterly loss since its financial restructuring in 2014, with the 2Q 2023 net loss reaching $213m. Zim took a $51m after-tax charge in the quarter for the redelivery of 4 containerships that were previously part of a sale and leaseback transaction as it struggles to cope with excess capacity. Zim’s woes were exacerbated by its unfavourable trade mix, with the unprofitable Transpacific and Intra-Asia (and Australia) routes accounting for 38% and 28% respectively of Zim’s total liftings, while it is under-exposed on the Asia-Med, Atlantic and Latin America that were still profitable during the 2nd quarter. Zim’s 2Q EBIT margin of -11.2% places it at the bottom of the earnings league table comprising of 10 of the top 12 carriers, with Zim the worst of the 3 carriers that dropped into loss making territory along with Wan Hai (net loss of $76m) and Yang Ming (net loss of $4m).

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year