MARKET BRIEF – 2022 WEEK 9

Freight rates remained soft last week as carriers were unable to push through the 1 March rate increases, with the SCFI recording its 8th consecutive weekly drop. Volumes remain soft with carriers still hoping for a pick up in demand in late March/early April in order to push for the next round of rate increases.

Port congestion remains steady, with the Ukraine-Russia conflict not adding materially to congestion in the Med and European ports. US congestion dropped marginally due to improvements at LA but congestion worsened in Vancouver and Oakland while USEC ports are mostly flat. Activity in Asia is picking up especially in South China but a stronger rebound is required to lift rates in the coming weeks. Congestion in Australia is rising due to impact of recent floods.

“Right now, three global alliances, made up entirely of foreign companies, control almost all of ocean freight shipping, giving them power to raise prices for American businesses and consumers, while threatening our national security and economic competitiveness.”

US White House statement 28 February 2022

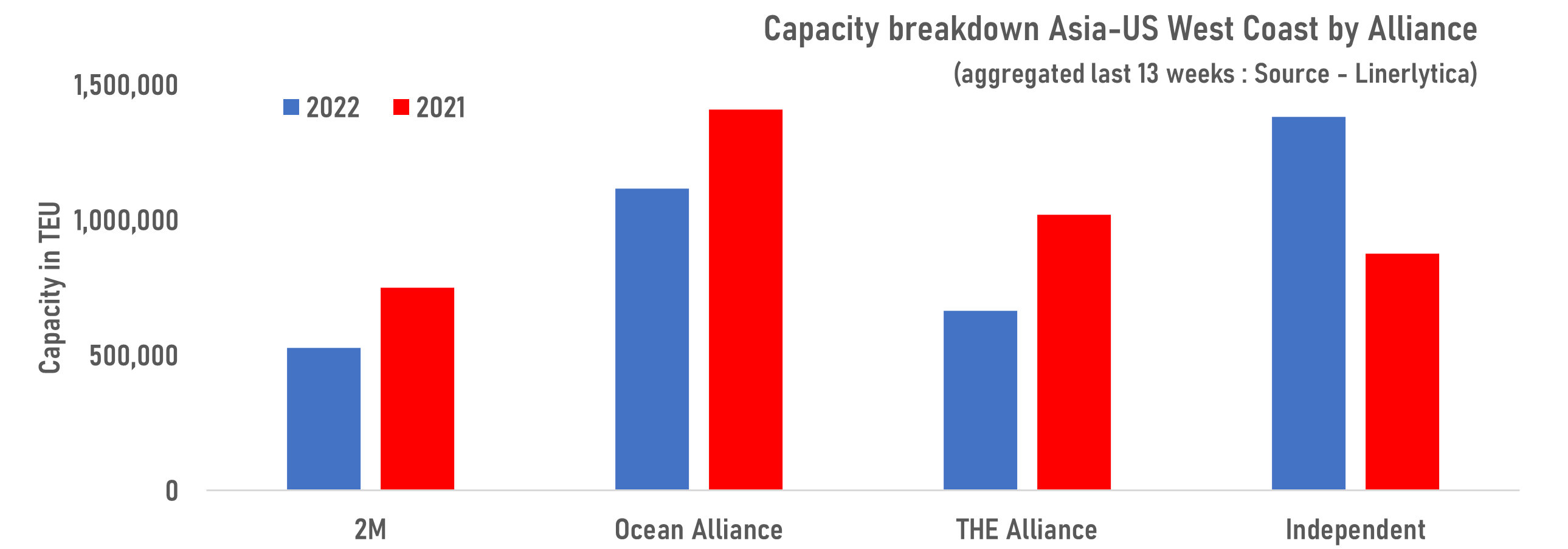

Blaming carrier alliances for the ocean freight rate inflation is misguided, as there is clear evidence that competition on the Transpacific routes have increased with 12 new independent carriers entering the trade since 2020. 37% of total transpacific capacity to the US West Coast is currently operated outside of the 3 global alliances. Independently operated capacity on this route has increased by 58% while capacity operated within the 3 global alliances shrank by 27% over the last 12 months.

Discount offer at $1,200 p.a. before end of March