Freight rates continued their spectacular collapse last week despite the severe port congestion that has built up in North Asia due to Typhoon Muifa, with the SCFI slipping by 33% within the past 4 weeks and down 50% year on year. Vessel utilisation on head haul routes have continued to drop despite shortfalls in ship departures, with carriers lacking resolve to remove excess vessel capacity in the market beyond ad hoc blank sailings that have been ineffective in curbing the rate drops.

Containership charter rates are finally catching up on the decline as the availability of open ships is rising rapidly and short term fixtures are no longer able to command any premiums over longer term commitments with further sharp rate corrections expected over the coming weeks.

Jonathan Lee

Jonathan Lee

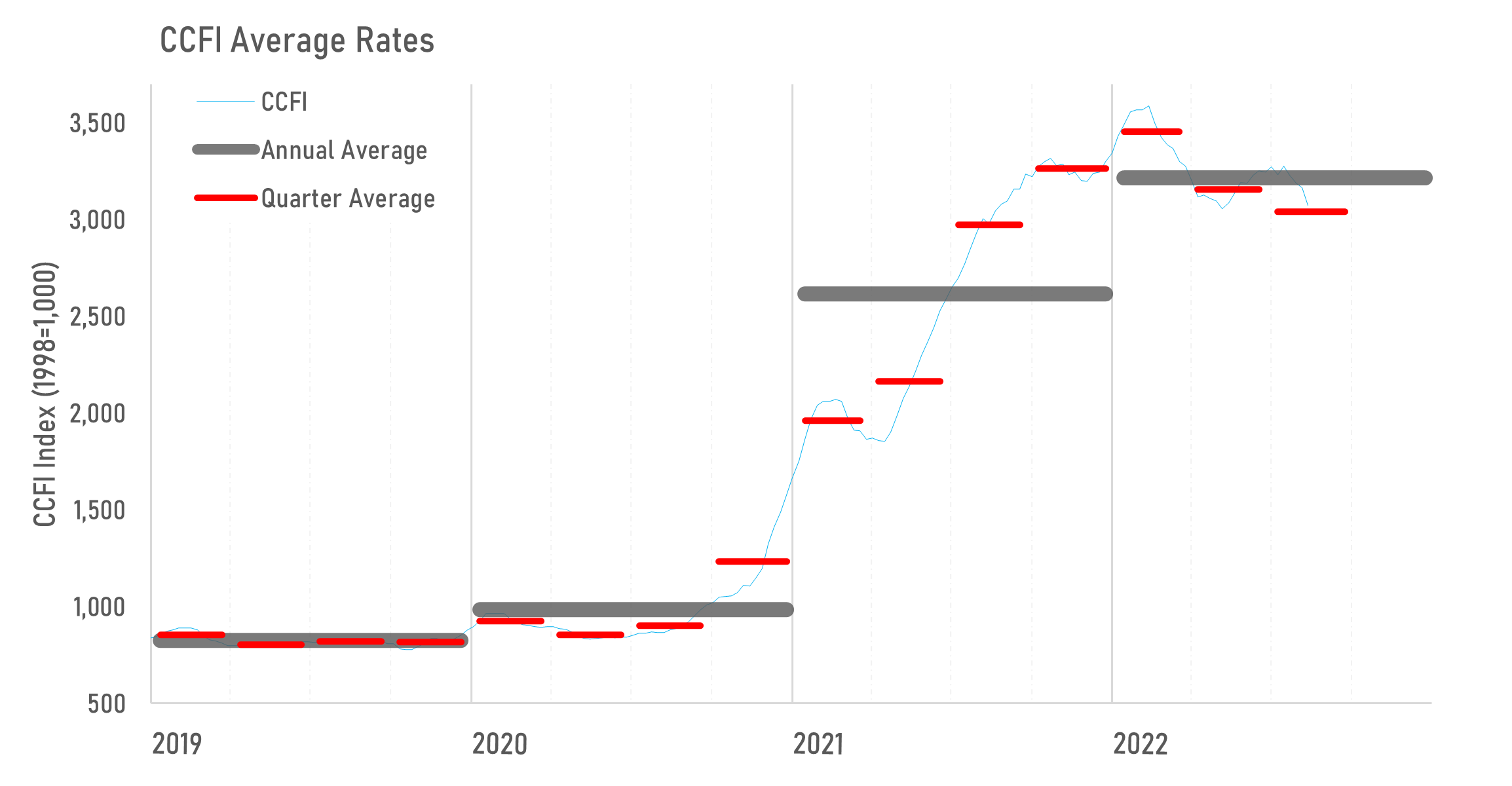

Carriers’ earnings are still well protected in the 3rd quarter despite the spectacular collapse in spot freight rates. The CCFI, which measures the average rates for shipments out of China (including contract rates), has slipped by 27% from the peak earlier this year but it remains well above the historical average. Average CCFI rates in the 3rd quarter is down by -3.7% against 2Q 2022 and -12.0% against 1Q 2022 but is still up marginally by +2.2% against 3Q 2021. However, 4Q earnings is now expected to slip sharply downwards as spot rates continue to tumble while full year contract rates are renegotiated downwards as carriers are increasingly desperate to protect customer volumes.

Weekly Market Pulse: US$1,500 per year