COSCO registered a particularly sharp QoQ drop in the EBIT margin during 21Q4 compared to its peers. However, at the cash flow level, COSCO’s operating profit improved from 54% in 21Q3 to 55% in 21Q4, which suggested much of the EBIT margin squeeze during 21Q4 was due to non-cash items.

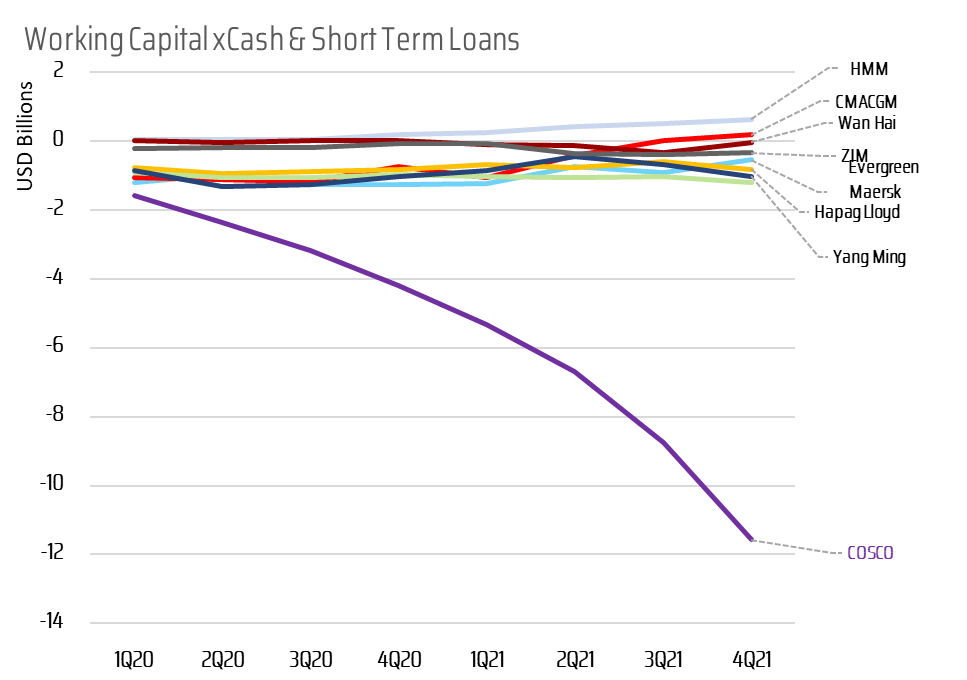

Looking at the working capital account, COSCO’s working capital has been falling continuously during the past 24 months due to mainly increase in account payables. In other words, COSCO may be able to defer payment of the expenses booked in each reporting period or some of the expenses are just provisions for the future cash outflow.

Working capital for a business usually grows with the size of a business. Since freight rate instead of volume was the main driver during the recent up cycle, working capital account see little changes for most of the liners except for COSCO.