The US East Coast dockworkers’ strike ended after the ILA agreed a 61.5% wage hike over 6 years, far in excess of the 32% increase that the ILWU secured for their 2022-2028 US West Coast master contract. Although congestion at East Coast ports surged to their highest levels since 2022 at the end of the 3-day strike, the vessel queue is clearing up quickly after all the affected ports resumed operations on Friday.

With the USEC uncertainty now out of the way, freight rates are poised to resume their decline after the Chinese Golden Week holidays as excess capacity continues to build up as blanked sailings are reduced this year. The weakness has not spilled over to the charter market with carriers still intent on securing tonnage as attention shifts to the launch of the new alliance networks in February.

Johnson Leung

Johnson Leung

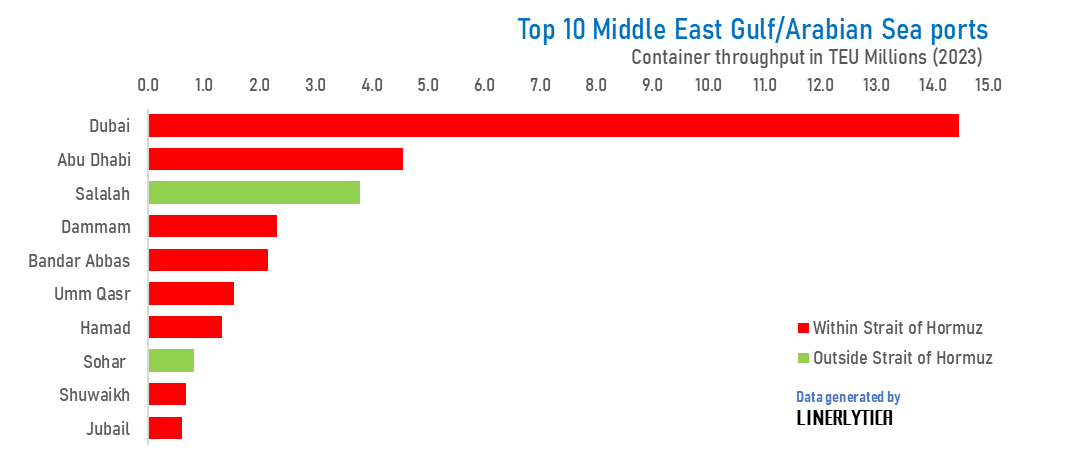

Impact of Strait of Hormuz disruption on the container market

The escalation of the Iran-Israel conflict in the Middle East has sparked fears of a potential disruption to vessel traffic in the Strait of Hormuz. The impact on the container markets will be far less severe compared to the tanker and LNG markets, as the Middle East Gulf is mostly an import market with very little exports of any strategic importance that are shipped in containers.

Middle East Gulf ports located north of the Strait of Hormuz handled a total of 29m teu of containers in 2023, accounting for 3.2% of global volumes. The 2 main UAE ports of Dubai and Abu Dhabi account for two-thirds of the total Gulf ports’ throughput and will be most badly affected by a potential closure of the Strait of Hormuz along with ports in Bahrain, Kuwait, Iran, Irag, Qatar and the eastern ports of Saudi Arabia, while the ports of Salalah, Sohar and Khor Fakkan will be the only main ports that can continue to function in the region.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year