US recession fears dominate the market this week, with the SCFI dropping for the 4th consecutive week on weakening capacity utilisation. Rates to the US West Coast have registered the sharpest drops and even though carriers are still pushing for a mid-August transpacific rate hike, market sentiment continues to weaken. Rates to North Europe are holding up relatively better, with capacity still constrained by both Red Sea diversions and the recent rise in port congestion that has affected ports in the Asia-Europe corridor more severely.

Tensions in the Middle East continues to escalate, with another Houthi attack on a containership last week despite having no Israeli connections. Effective capacity continues to be constrained by the Red Sea diversions, with Maersk and ONE both raising their full year earnings guidance, even as MSC continues to push ahead with its latest newbuilding plans as it continues to widen the capacity gap to their main rivals.

Johnson Leung

Johnson Leung

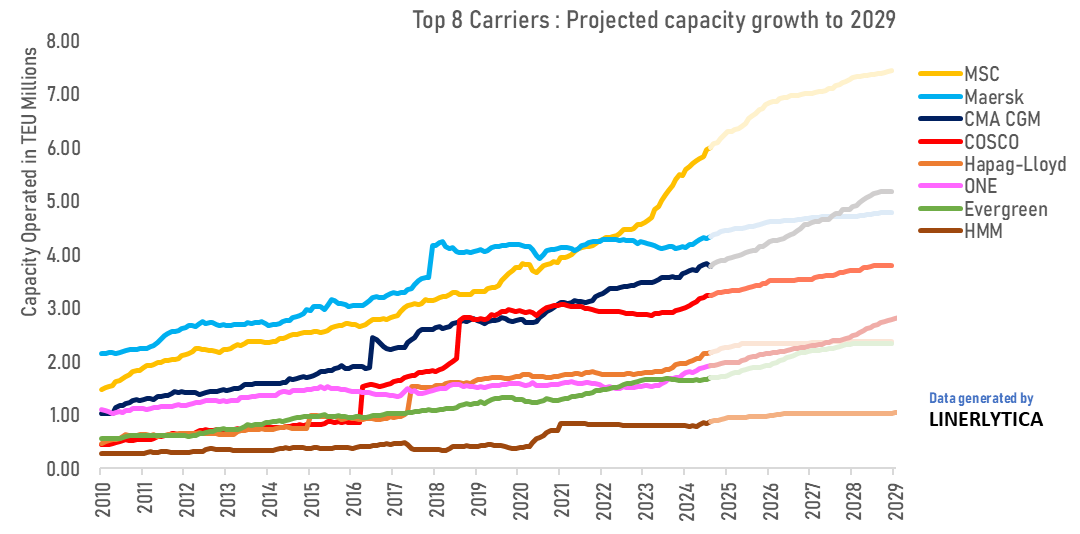

MSC builds unassailable lead with planned new ship orders

MSC’s planned newbuilding orders will bring its overall fleet to 7.5m TEU by the end of 2028 as it continues to widen the gap with their main rivals. The latest MSC orders is expected to include 10 units of 21,000 teu at Hantong, as well as a series of 12,000 teu units at Rongsheng and 11,000 teu units at Penglai Jinglu to be delivered from 2027. Although CMA CGM’s new vessel delivery pipeline will allow it to surpass Maersk by 2027, it will still trail MSC by more than 2m teu by the end of 2028.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year