The SCFI retreated last week by 1.6% after 14 consecutive weekly gains in a further sign that the market has peaked. While demand remains firm, supply has also risen with capacity injections most notably in the Indian subcontinent, Latin America and US West Coast routes where freight rates are the most lucrative currently. This has capped freight rate increases on those routes, but overall capacity utilisation remains tight, with rates still rising on the Asia-North Europe route as schedule disruptions due to port congestion and adverse weather conditions continue to affect the market. The charter market remains effectively sold out for the larger vessel segments until next year.

The FMC’s request for additional information regarding the Gemini Cooperation Agreement on 12 July will delay the effective date of the new alliance partnership of Maersk and Hapag-Lloyd. However, as the new alliance services are only scheduled to start in February 2025, there is still sufficient time for 2 partners to obtain the necessary regulatory approvals.

Johnson Leung

Johnson Leung

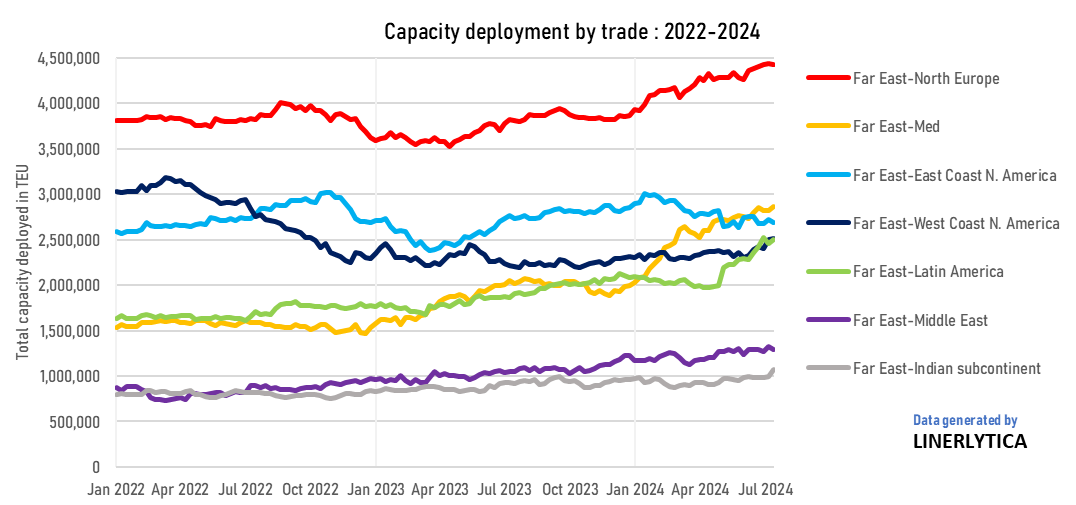

Recent capacity additions have put cap on freight rate increases

The Far East to the Indian Subcontinent, Latin America and US West Coast routes have seen a significant increase in new capacity injections in the last month, with capacity rising by 9.0%, 6.0% and 4.7% respectively with a slew new services and extra loaders added since June. These capacity additions will continue through August, keeping the charter market tight as carriers are still short of tonnage needed on these routes. However, the incremental capacity added has put a cap to recent freight rate increases, with carriers forced to roll back some of their rate hikes as the SCFI recorded its first week on week decline since April.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year