Renewed apprehension over a Middle East ceasefire and signs that freight rates may have peaked spooked the jittery container shipping equity and freight futures markets on 8 July despite continued advances in the SCFI and charter rate indices last week.

Although carriers successfully pushed ahead with the 1 July rate hikes, cracks have appeared on their ability to secure further rate increases as the additional capacity introduced into the US West Coast, North Europe, South America and Middle East have alleviated the capacity pressure on these routes. Despite this, freight rates will remain elevated until the end of the peak season which could last until September.

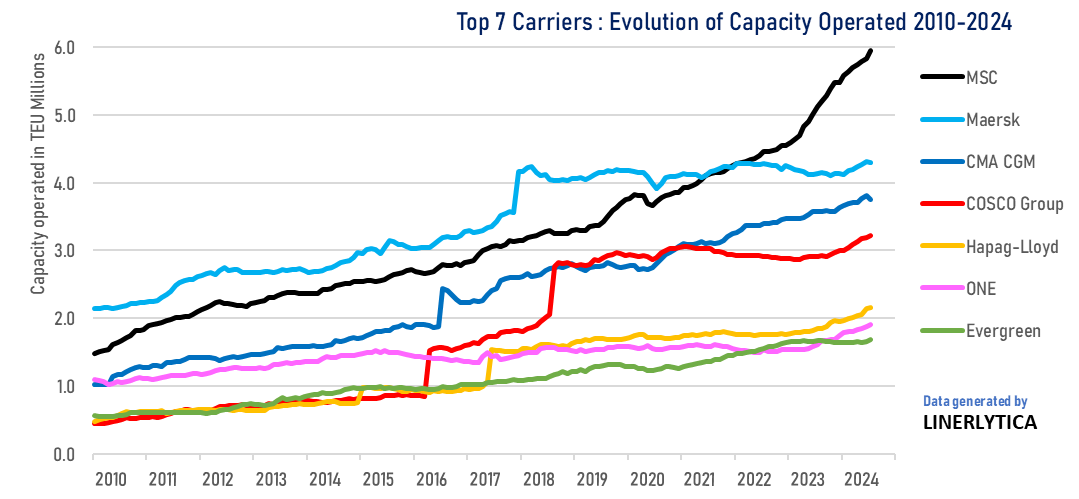

Maersk has hinted on a reversal of its strategy that could see a return to growth for its liner business with increased vessel charters and new ship orders as it seeks to close the lead that MSC has built.

Johnson Leung

Johnson Leung

Maersk set to reverse course after failed Schenker bid

With the rest of its main rivals pushing ahead with their capacity expansion plans, Maersk has been stagnant with its capacity operated capped at 4.3m TEU since 2017 as the Group pursued its logistics integrator strategy. This is set to change as Maersk stated last week that it will be “doing whatever it reasonably can to bring supply in line with businesses’ demand for capacity”, as it hints to an imminent reversal of its self-imposed capacity cap. The move follows Maersk’s withdrawal from its bid to acquire Schenker on 1 July 2024 citing integration challenges, in a further sign of a shift in Maersk’s focus back to the liner business.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year