The container market stepped up further with SCFI spot rates surging by a further 6.9% while EC freight futures for 2025 contracts registered strong gains on rising conviction that the Red Sea crisis will last through next year. Charter rates continues to set higher benchmarks although carriers remain hesitant to commit to forward positions for ships that are coming open at the end this year and early 2025.

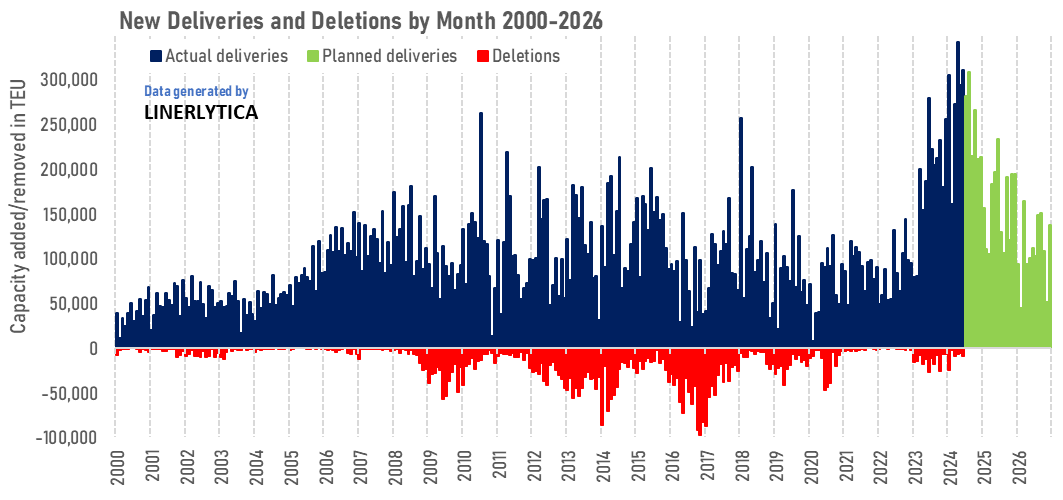

The Latin America, USWC and North Europe markets continue to absorb most of the incremental capacity and carrier will soon face resistance to further rate hikes due to the impact of the new capacity additions. But there will be some relieve on the supply side as the pace of new vessel deliveries start to slow from the 3rd quarter onwards after the frenetic pace of deliveries saw 950,000 teu delivered in the last 3 months.

Johnson Leung

Johnson Leung

Peak newbuilding delivery phase has passed as container fleet reaches 30m teu milestone

The global containership fleet has exceeded the 30m teu milestone for the first time with 51 new containerships delivered in June, bringing the total number of ships delivered in the first 6 months of this year to 271 units for 1.68m teu. A further 1.49m teu is scheduled for delivery later in the 2nd half of the year with only minimal slippages expected.

The 2nd quarter is the peak of the current delivery cycle, with an average monthly delivery rate of 315,000 teu at almost 2 new ships joining the fleet daily. The average monthly delivery rate will fall to 260,000 teu in the 3rd quarter and 230,000 teu in the 4th quarter.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year