The container market remains red hot with short term charter rates breaching the $150,000 per day benchmark and spot freight rates rising above the $8,000/feu level, setting new highs not seen since the end of 2022. New services out of Asia continue at a rapid pace, led by the Mexico route with 6 new services launched since May, followed closely by 5 new services to the US West Coast and 3 new services to North Europe. There is clearly insufficient tonnage available to keep up with the rampant demand, with the Cape diversions and rising port congestion effectively removing more than 2m teu of vessel capacity from the global fleet since December last year.

The tight market conditions has not stopped MSC from widening its lead at the top of the market as its operated fleet will hit the 6m TEU mark in July, boosted by capacity additions from newbuildings and second hand vessel acquisitions.

Johnson Leung

Johnson Leung

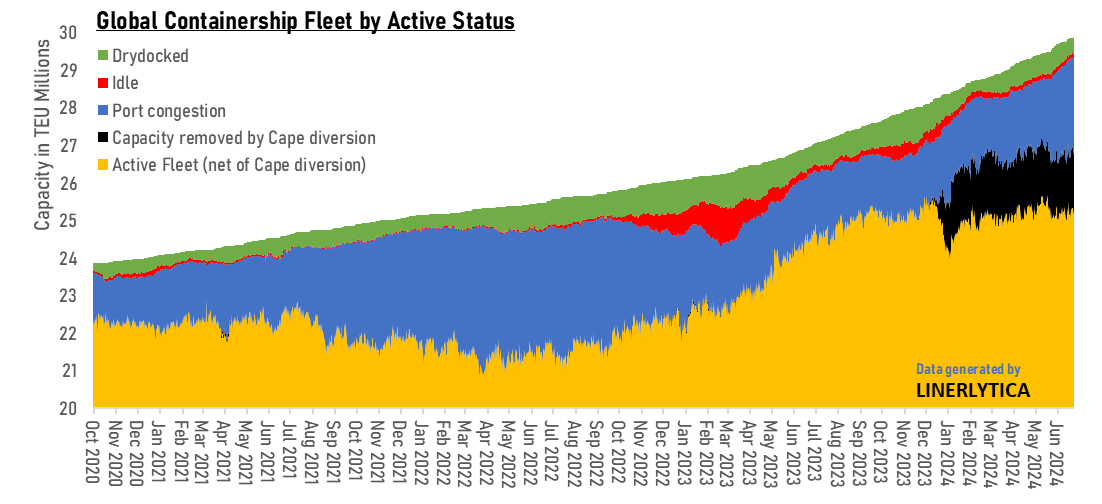

Cape diversion and port congestion keep effective fleet growth in check

New containership deliveries has reached 1.62m TEU this year but there remains a shortage of ships globally with freight and charter rates continuing to surge ahead as the market enters the traditional summer peak season.

The vessel diversions from the Red Sea to the Cape route has effectively removed more than 1.6m TEU from the market since the beginning of December while the recent increase in port congestion has taken out a further 0.5m TEU of vessel capacity from circulation as the active fleet currently stands at just over 25m TEU, which is below the 25.5m TEU at its peak in December 2023.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year